What Happens When a Country Has an Absolute Advantage in All Goods

Intra-industry Trade between Similar Economies

The Benefits of Reducing Barriers to International Trade

Measuring Trade Balances

Trade Balances in Historical and International Context

Trade Balances and Flows of Financial Capital

The National Saving and Investment Identity

The Pros and Cons of Trade Deficits and Surpluses

The Difference between Level of Trade and the Trade Balance

6.1 Introduction

We live in a global marketplace. The food on your table might include fresh fruit from Chile, cheese from France, and bottled water from Scotland. Your wireless phone might have been made in Taiwan or Korea. The clothes you wear might be designed in Italy and manufactured in China. The toys you give to a child might have come from India. The car you drive might come from Japan, Germany, or Korea. The gasoline in the tank might be refined from crude oil from Saudi Arabia, Mexico, or Nigeria. As a worker, if your job is involved with farming, machinery, airplanes, cars, scientific instruments, or many other technology-related industries, the odds are good that a hearty proportion of the sales of your employer—and hence the money that pays your salary—comes from export sales. We are all linked by international trade, and the volume of that trade has grown dramatically in the last few decades.

The first wave of globalization started in the nineteenth century and lasted up to the beginning of World War I. Over that time, global exports as a share of global GDP rose from less than 1% of GDP in 1820 to 9% of GDP in 1913. As the Nobel Prize-winning economist Paul Krugman of Princeton University wrote in 1995:

It is a late-twentieth-century conceit that we invented the global economy just yesterday. In fact, world markets achieved an impressive degree of integration during the second half of the nineteenth century. Indeed, if one wants a specific date for the beginning of a truly global economy, one might well choose 1869, the year in which both the Suez Canal and the Union Pacific railroad were completed. By the eve of the First World War steamships and railroads had created markets for standardized commodities, like wheat and wool, that were fully global in their reach. Even the global flow of information was better than modern observers, focused on electronic technology, tend to realize: the first submarine telegraph cable was laid under the Atlantic in 1858, and by 1900 all of the world’s major economic regions could effectively communicate instantaneously.

This first wave of globalization crashed to a halt early in the twentieth century. World War I severed many economic connections. During the Great Depression of the 1930s, many nations misguidedly tried to fix their own economies by reducing foreign trade with others. World War II further hindered international trade. Global flows of goods and financial capital were rebuilt only slowly after World War II. It was not until the early 1980s that global economic forces again became as important, relative to the size of the world economy, as they were before World War I.

Figure 6.1: While the iPhone is readily recognized as an Apple product, 26% of the component costs in it come from components made by rival phone-maker, Samsung. In international trade, there are often “conflicts” like this as each country or company focuses on what it does best. (Credit: modification of work by Yutaka Tsutano Creative Commons)

Note

JUST WHOSE IPHONE IS IT?

The iPhone is a global product. Apple does not manufacture the iPhone components, nor does it assemble them. The assembly is done by Foxconn Corporation, a Taiwanese company, at its factory in Sengzhen, China. But, Samsung, the electronics firm and competitor to Apple, actually supplies many of the parts that make up an iPhone—representing about 26% of the costs of production. That means, that Samsung is both the biggest supplier and biggest competitor for Apple.

Why do these two firms work together to produce the iPhone? To understand the economic logic behind international trade, you have to accept, as these firms do, that trade is about mutually beneficial exchange. Samsung is one of the world’s largest electronics parts suppliers. Apple lets Samsung focus on making the best parts, which allows Apple to concentrate on its strength—designing elegant products that are easy to use. If each company (and by extension each country) focuses on what it does best, there will be gains for all through trade.

6.2 Absolute and Comparative Advantage

Section Learning Objectives

Define absolute advantage, comparative advantage, and opportunity costs

Explain the gains of trade created when a country specializes

The American statesman Benjamin Franklin (1706–1790) once wrote: “No nation was ever ruined by trade.” Many economists would express their attitudes toward international trade in an even more positive manner. The evidence that international trade confers overall benefits on economies is pretty strong. Trade has accompanied economic growth in the United States and around the world. Many of the national economies that have shown the most rapid growth in the last several decades—for example, Japan, South Korea, China, and India—have done so by dramatically orienting their economies toward international trade. There is no modern example of a country that has shut itself off from world trade and yet prospered. To understand the benefits of trade, or why we trade in the first place, we need to understand the concepts of comparative and absolute advantage.

In 1817, David Ricardo, a businessman, economist, and member of the British Parliament, wrote a treatise called On the Principles of Political Economy and Taxation. In this treatise, Ricardo argued that specialization and free trade benefit all trading partners, even those that may be relatively inefficient. To see what he meant, we must be able to distinguish between absolute and comparative advantage.

A country has an absolute advantage over another country in producing a good if it uses fewer resources to produce that good. Absolute advantage can be the result of a country’s natural endowment. For example, extracting oil in Saudi Arabia is pretty much just a matter of “drilling a hole.” Producing oil in other countries can require considerable exploration and costly technologies for drilling and extraction—if they have any oil at all. The United States has some of the richest farmland in the world, making it easier to grow corn and wheat than in many other countries. Guatemala and Colombia have climates especially suited for growing coffee. Chile and Zambia have some of the world’s richest copper mines. As some have argued, “geography is destiny.” Chile will provide copper and Guatemala will produce coffee, and they will trade. When each country has a product others need and it can produce it with fewer resources in one country than in another, then it is easy to imagine all parties benefitting from trade. However, thinking about trade just in terms of geography and absolute advantage is incomplete. Trade really occurs because of comparative advantage.

Recall from the chapter Choice in a World of Scarcity that a country has a comparative advantage when it can produce a good at a lower cost in terms of other goods. The question each country or company should be asking when it trades is this: “What do we give up to produce this good?” It should be no surprise that the concept of comparative advantage is based on this idea of opportunity cost from Choice in a World of Scarcity. For example, if Zambia focuses its resources on producing copper, it cannot use its labor, land and financial resources to produce other goods such as corn. As a result, Zambia gives up the opportunity to produce corn. How do we quantify the cost in terms of other goods? Simplify the problem and assume that Zambia just needs labor to produce copper and corn. The companies that produce either copper or corn tell you that it takes two hours to mine a ton of copper and one hour to harvest a bushel of corn. This means the opportunity cost of producing a ton of copper is two bushels of corn. The next section develops absolute and comparative advantage in greater detail and relates them to trade.

6.2.1 A Numerical Example of Absolute and Comparative Advantage

Video - Comparative Advantage

Consider a hypothetical world with two countries, Saudi Arabia and the United States, and two products, oil and corn. Further assume that consumers in both countries desire both these goods. These goods are homogeneous, meaning that consumers/producers cannot differentiate between corn or oil from either country. There is only one resource available in both countries, labor hours. Saudi Arabia can produce oil with fewer resources, while the United States can produce corn with fewer resources. Table 17.1 illustrates the advantages of the two countries, expressed in terms of how many hours it takes to produce one unit of each good.

Table 6.1: How Many Hours It Takes to Produce Oil and Corn

Country

Oil (hours per barrel)

Corn (hours per bushel)

Saudi Arabia

1

4

United States

2

1

In Table 17.1, Saudi Arabia has an absolute advantage in producing oil because it only takes an hour to produce a barrel of oil compared to two hours in the United States. The United States has an absolute advantage in producing corn.

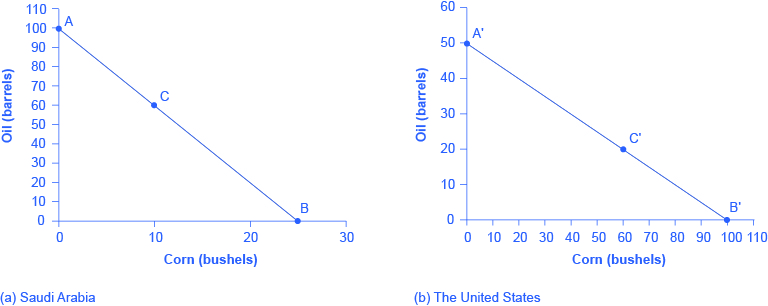

To simplify, let’s say that Saudi Arabia and the United States each have 100 worker hours (see Table 6.2). Figure 6.2 illustrates what each country is capable of producing on its own using a production possibility frontier (PPF) graph. Recall from Choice in a World of Scarcity that the production possibilities frontier shows the maximum amount that each country can produce given its limited resources, in this case workers, and its level of technology.

Table 6.2: Production Possibilities before Trade

Country

Oil Prod. using 100 worker hours (barrels)

Corn Prod. using 100 worker hours (bushels)

Saudi Arabia

100 or

25

United States

50 or

100

Figure 6.2: Production Possibilities Frontiers. Panel (a) Saudi Arabia can produce 100 barrels of oil at maximum and zero corn (point A), or 25 bushels of corn and zero oil (point B). It can also produce other combinations of oil and corn if it wants to consume both goods, such as at point C. Here it chooses to produce/consume 60 barrels of oil, leaving 40 work hours that to allocate to produce 10 bushels of corn, using the data in Table. (b) If the United States produces only oil, it can produce, at maximum, 50 barrels and zero corn (point A'), or at the other extreme, it can produce a maximum of 100 bushels of corn and no oil (point B'). Other combinations of both oil and corn are possible, such as point C'. All points above the frontiers are impossible to produce given the current level of resources and technology.

These graphs illustrate the production possibilities frontier before trade for both Saudi Arabia and the United States using the data in the table titled “Production Possibilities before Trade”. The x-axis plots corn production, measured by bushels, and the y-axis plots oil, in terms of barrels. All points above the frontier are impossible to produce given the current level of resources and technology.

(a) Saudi Arabia can produce 100 barrels of oil at maximum and zero corn (point A), or 25 bushels of corn and zero oil (point B). It can also produce other combinations of oil and corn if it wants to consume both goods, such as at point C. Here it chooses to produce/consume 60 barrels of oil, leaving 40 work hours that to allocate to produce 10 bushels of corn, using the data in Table.

(b) If the United States produces only oil, it can produce, at maximum, 50 barrels and zero corn (point A'), or at the other extreme, it can produce a maximum of 100 bushels of corn and no oil (point B'). Other combinations of both oil and corn are possible, such as point C'. All points above the frontiers are impossible to produce given the current level of resources and technology.

Arguably Saudi and U.S. consumers desire both oil and corn to live. Let’s say that before trade occurs, both countries produce and consume at point C or C'. Thus, before trade, the Saudi Arabian economy will devote 60 worker hours to produce oil, as Table shows. Given the information in Table, this choice implies that it produces/consumes 60 barrels of oil. With the remaining 40 worker hours, since it needs four hours to produce a bushel of corn, it can produce only 10 bushels. To be at point C', the U.S. economy devotes 40 worker hours to produce 20 barrels of oil and it can allocate the remaining worker hours to produce 60 bushels of corn.

Table 6.3: Production before Trade

Country

Oil Production (barrels)

Corn Production (bushels)

Saudi Arabia (C)

60

10

United States (C')

20

60

Total World Production

80

70

The slope of the production possibility frontier illustrates the opportunity cost of producing oil in terms of corn. Using all its resources, the United States can produce 50 barrels of oil or 100 bushels of corn; therefore, the opportunity cost of one barrel of oil is two bushels of corn—or the slope is 1/2. Thus, in the U.S. production possibility frontier graph, every increase in oil production of one barrel implies a decrease of two bushels of corn. Saudi Arabia can produce 100 barrels of oil or 25 bushels of corn.

The opportunity cost of producing one barrel of oil is the loss of 1/4 of a bushel of corn that Saudi workers could otherwise have produced. In terms of corn, notice that Saudi Arabia gives up the least to produce a barrel of oil. Table 6.4 summarizes these calculations.

Table 6.4: Opportunity Cost and Comparative Advantage

Country

Opportunity cost of one unit: Oil

| (in terms of corn)

Opportunity cost of one unit: Corn

| (in terms of oil)

Saudi Arabia

\(\frac{1}{4}\)

4

United States

2

\(\frac{1}{2}\)

Again recall that we defined comparative advantage as the opportunity cost of producing goods. Since Saudi Arabia gives up the least to produce a barrel of oil, (\(\frac{1}{4} < 2\) in Table 6.4) it has a comparative advantage in oil production. The United States gives up the least to produce a bushel of corn, so it has a comparative advantage in corn production.

In this example, there is symmetry between absolute and comparative advantage. Saudi Arabia needs fewer worker hours to produce oil (absolute advantage, see Table 6.3), and also gives up the least in terms of other goods to produce oil (comparative advantage, see Table 6.4). Such symmetry is not always the case, as we will show after we have discussed gains from trade fully, but first, read the following Clear It Up feature to make sure you understand why the PPF line in the graphs is straight.

Note

CAN A PRODUCTION POSSIBILITY FRONTIER BE STRAIGHT?

When you first met the production possibility frontier (PPF) in the chapter on Choice in a World of Scarcity we drew it with an outward-bending shape. This shape illustrated that as we transferred inputs from producing one good to another—like from education to health services—there were increasing opportunity costs. In the examples in this chapter, we draw the PPFs as straight lines, which means that opportunity costs are constant. When we transfer a marginal unit of labor away from growing corn and toward producing oil, the decline in the quantity of corn and the increase in the quantity of oil is always the same.

In reality this is possible only if the contribution of additional workers to output did not change as the scale of production changed. The linear production possibilities frontier is a less realistic model, but a straight line simplifies calculations. It also illustrates economic themes like absolute and comparative advantage just as clearly.

6.2.2 Gains from Trade

Consider the trading positions of the United States and Saudi Arabia after they have specialized and traded in Table 6.5. Before trade, Saudi Arabia produces/consumes 60 barrels of oil and 10 bushels of corn. The United States produces/consumes 20 barrels of oil and 60 bushels of corn. Given their current production levels, if the United States can trade an amount of corn fewer than 60 bushels and receives in exchange an amount of oil greater than 20 barrels, it will gain from trade.

With trade, the United States can consume more of both goods than it did without specialization and trade. (Recall that the chapter Welcome to Economics! defined specialization as it applies to workers and firms. Economists also use specialization to describe the occurrence when a country shifts resources to focus on producing a good that offers comparative advantage.) Similarly, if Saudi Arabia can trade an amount of oil less than 60 barrels and receive in exchange an amount of corn greater than 10 bushels, it will have more of both goods than it did before specialization and trade. Table illustrates the range of trades that would benefit both sides.

Table 6.5: The Range of Trades That Benefit Both the United States and Saudi Arabia

The U.S. economy, after specialization,

| will benefit if it: ,

The Saudi Arabian economy,

after specialization will benefit

| if it:

Exports no more than 60 bushels of corn

Imports at least 10 bushels of corn

Imports at least 20 barrels of oil

Exports less than 60 barrels of oil

The underlying reason why trade benefits both sides is rooted in the concept of opportunity cost, as the following Clear It Up feature explains. If Saudi Arabia wishes to expand domestic production of corn in a world without international trade, then based on its opportunity costs it must give up four barrels of oil for every one additional bushel of corn. If Saudi Arabia could find a way to give up less than four barrels of oil for an additional bushel of corn (or equivalently, to receive more than one bushel of corn for four barrels of oil), it would be better off.

Note

WHAT ARE THE OPPORTUNITY COSTS AND GAINS FROM TRADE?

The range of trades that will benefit each country is based on the country’s opportunity cost of producing each good. The United States can produce 100 bushels of corn or 50 barrels of oil. For the United States, the opportunity cost of producing one barrel of oil is two bushels of corn. If we divide the numbers above by 50, we get the same ratio: one barrel of oil is equivalent to two bushels of corn, or (100/50 = 2 and 50/50 = 1).

In a trade with Saudi Arabia, if the United States is going to give up 100 bushels of corn in exports, it must import at least 50 barrels of oil to be just as well off. Clearly, to gain from trade it needs to be able to gain more than a half barrel of oil for its bushel of corn—or why trade at all?

Recall that David Ricardo argued that if each country specializes in its comparative advantage, it will benefit from trade, and total global output will increase. How can we show gains from trade as a result of comparative advantage and specialization? Table 6.6 shows the output assuming that each country specializes in its comparative advantage and produces no other good. This is 100% specialization. Specialization leads to an increase in total world production. (Compare the total world production in Table 6.2 to that in Table 6.6.)

Table 6.6: How Specialization Expands Output

Country

Quantity produced after 100%

| specialization — Oil (barrels)

Quantity produced after 100%

| specialization — Corn (bushels)

Saudi Arabia

100

0

United States

0

100

World Production

100

100

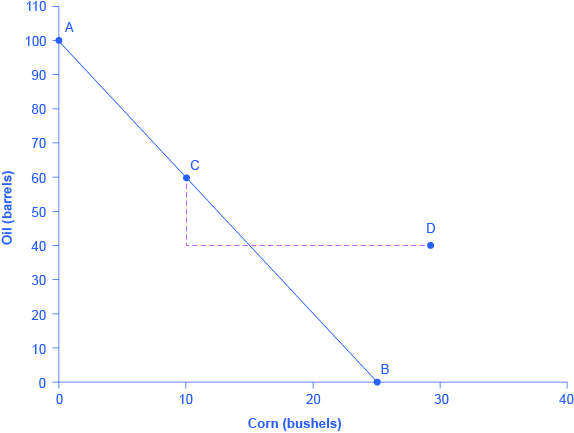

What if we did not have complete specialization, as in Table 6.6? Would there still be gains from trade? Consider another example, such as when the United States and Saudi Arabia start at C and C', respectively, as Figure 6.3 shows. Consider what occurs when trade is allowed and the United States exports 20 bushels of corn to Saudi Arabia in exchange for 20 barrels of oil.

Figure 6.3: Production Possibilities Frontier in Saudi Arabia. Trade allows a country to go beyond its domestic production-possibility frontier

On this graph, Corn is on the x-axis with a maximum production of 25 bushels and oil is on the y-axis with a maximum production of 100 barrels. Saudi Arabia begins producing and consuming at point C (coordinates 10, 60). If the “trade price” is 20 barrels of oil for 20 bushels of corn, the Saudis end up at D (coordinates 30, 40).

Starting at point C, which shows Saudi oil production of 60, reduce Saudi oil domestic oil consumption by 20, since 20 is exported to the United States and exchanged for 20 units of corn. This enables Saudi to reach point D, where oil consumption is now 40 barrels and corn consumption has increased to 30 (see Figure). Notice that even without 100% specialization, if the “trading price,” in this case 20 barrels of oil for 20 bushels of corn, is greater than the country’s opportunity cost, the Saudis will gain from trade. Since the post-trade consumption point D is beyond its production possibility frontier, Saudi Arabia has gained from trade.

Key Concepts and Summary

A country has an absolute advantage in those products in which it has a productivity edge over other countries; it takes fewer resources to produce a product.

A country has a comparative advantage when it can produce a good at a lower cost in terms of other goods.

Countries that specialize based on comparative advantage gain from trade.

Self-Check Questions

True or False: The source of comparative advantage must be natural elements like climate and mineral deposits. Explain.

Brazil can produce 100 pounds of beef or 10 autos. In contrast the United States can produce 40 pounds of beef or 30 autos. Which country has the absolute advantage in beef? Which country has the absolute advantage in producing autos? What is the opportunity cost of producing one pound of beef in Brazil? What is the opportunity cost of producing one pound of beef in the United States?

In France it takes one worker to produce one sweater, and one worker to produce one bottle of wine. In Tunisia it takes two workers to produce one sweater, and three workers to produce one bottle of wine. Who has the absolute advantage in production of sweaters? Who has the absolute advantage in the production of wine? How can you tell?

What is absolute advantage? What is comparative advantage?

Under what conditions does comparative advantage lead to gains from trade?

What factors does Paul Krugman identify that supported expanding international trade in the 1800s?

Are differences in geography behind the differences in absolute advantages?

Why does the United States not have an absolute advantage in coffee?

Look at Exercise. Compute the opportunity costs of producing sweaters and wine in both France and Tunisia. Who has the lowest opportunity cost of producing sweaters and who has the lowest opportunity cost of producing wine? Explain what it means to have a lower opportunity cost.

6.3 What Happens When a Country Has an Absolute Advantage in All Goods

Chapter Learning Objectives

Show the relationship between production costs and comparative advantage

Identify situations of mutually beneficial trade

Identify trade benefits by considering opportunity costs

What happens to the possibilities for trade if one country has an absolute advantage in everything? This is typical for high-income countries that often have well-educated workers, technologically advanced equipment, and the most up-to-date production processes. These high-income countries can produce all products with fewer resources than a low-income country. If the high-income country is more productive across the board, will there still be gains from trade? Good students of Ricardo understand that trade is about mutually beneficial exchange. Even when one country has an absolute advantage in all products, trade can still benefit both sides. This is because gains from trade come from specializing in one’s comparative advantage.

6.3.1 Production Possibilities and Comparative Advantage

Consider the example of trade between the United States and Mexico described in Table 6.7. In this example, it takes four U.S. workers to produce 1,000 pairs of shoes, but it takes five Mexican workers to do so. It takes one U.S. worker to produce 1,000 refrigerators, but it takes four Mexican workers to do so. The United States has an absolute advantage in productivity with regard to both shoes and refrigerators; that is, it takes fewer workers in the United States than in Mexico to produce both a given number of shoes and a given number of refrigerators.

Table 6.7: Resources Needed to Produce Shoes and Refrigerators

Country

Number of Workers needed

| to produce 1,000 units — Shoes

Number of Workers needed

| to produce 1,000 units — Refrigerators

United States

4 workers

1 worker

Mexico

5 workers

4 workers

Absolute advantage simply compares the productivity of a worker between countries. It answers the question, “How many inputs do I need to produce shoes in Mexico?” Comparative advantage asks this same question slightly differently. Instead of comparing how many workers it takes to produce a good, it asks, “How much am I giving up to produce this good in this country?” Another way of looking at this is that comparative advantage identifies the good for which the producer’s absolute advantage is relatively larger, or where the producer’s absolute productivity disadvantage is relatively smaller.

The United States can produce 1,000 shoes with four-fifths as many workers as Mexico (four versus five), but it can produce 1,000 refrigerators with only one-quarter as many workers (one versus four). So, the comparative advantage of the United States, where its absolute productivity advantage is relatively greatest, lies with refrigerators, and Mexico’s comparative advantage, where its absolute productivity disadvantage is least, is in the production of shoes.

6.3.2 Benefits from Specialization (The Ricardian Trade Model)

When nations increase production in their area of comparative advantage and trade with each other, both countries can benefit. Again, the production possibility frontier is a useful tool to visualize this benefit. This theory was developed by British Economist David Ricardo (1772--1823).

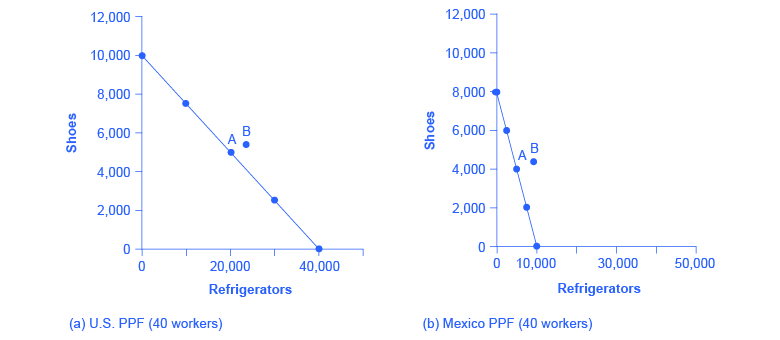

Consider a situation where the United States and Mexico each have 40 workers. For example, as Table 6.8 shows, if the United States divides its labor so that 40 workers are making shoes, then, since it takes four workers in the United States to make 1,000 shoes, a total of 10,000 shoes will be produced. (If four workers can make 1,000 shoes, then 40 workers will make 10,000 shoes). If the 40 workers in the United States are making refrigerators, and each worker can produce 1,000 refrigerators, then a total of 40,000 refrigerators will be produced.

Table 6.8: Production Possibilities before Trade with Complete Specialization

Country

Shoe Production — using 40 workers

Refrigerator Production — using 40 workers

U.S.

10,000 shoes or

40,000 refrigerators

Mexico

8,000 shoes or

10,000 refrigerators

As always, the slope of the production possibility frontier for each country is the opportunity cost of one refrigerator in terms of foregone shoe production–when labor is transferred from producing the latter to producing the former (see Figure 6.4).

Figure 6.4: Production Possibility Frontiers (a) With 40 workers, the United States can produce either 10,000 shoes and zero refrigerators or 40,000 refrigerators and zero shoes. (b) With 40 workers, Mexico can produce a maximum of 8,000 shoes and zero refrigerators, or 10,000 refrigerators and zero shoes. All other points on the production possibility line are possible combinations of the two goods that can be produced given current resources. Point A on both graphs is where the countries start producing and consuming before trade. Point B is where they end up after trade.

The graphs show two production possibility frontiers (PPFs) for the United States (graph a) and Mexico (graph b). The PPFs are linear. The x-axis plots refrigerators and the y-axis plots shoes. (a) With 40 workers, the United States can produce either 10,000 shoes and zero refrigerators or 40,000 refrigerators and zero shoes. (b) With 40 workers, Mexico can produce a maximum of 8,000 shoes and zero refrigerators, or 10,000 refrigerators and zero shoes. Point B is where they end up after trade.

Let’s say that, in the situation before trade, each nation prefers to produce a combination of shoes and refrigerators that is shown at point A. Table 6.9 shows the output of each good for each country and the total output for the two countries.

Table 6.9: Total Production at Point A before Trade

Country

Current Shoe Production

Current Refrigerator Production

U.S.

5,000

20,000

Mexico

4,000

5,000

Total

9,000

25,000

Continuing with this scenario, suppose that each country transfers some amount of labor toward its area of comparative advantage. For example, the United States transfers six workers away from shoes and toward producing refrigerators. As a result, U.S. production of shoes decreases by 1,500 units (6/4 × 1,000), while its production of refrigerators increases by 6,000 (that is, 6/1 × 1,000). Mexico also moves production toward its area of comparative advantage, transferring 10 workers away from refrigerators and toward production of shoes. As a result, production of refrigerators in Mexico falls by 2,500 (10/4 × 1,000), but production of shoes increases by 2,000 pairs (10/5 × 1,000). Notice that when both countries shift production toward each of their comparative advantages (what they are relatively better at), their combined production of both goods rises, as shown in Table 6.10.

The reduction of shoe production by 1,500 pairs in the United States is more than offset by the gain of 2,000 pairs of shoes in Mexico, while the reduction of 2,500 refrigerators in Mexico is more than offset by the additional 6,000 refrigerators produced in the United States.

Table 6.10: Shifting Production Toward Comparative Advantage Raises Total Output

Country

Shoe Production

Refrigerator Production

U.S.

3,500

26,000

Mexico

6,000

2,500

Total

9,500

28,500

This numerical example illustrates the remarkable insight of comparative advantage: even when one country has an absolute advantage in all goods and another country has an absolute disadvantage in all goods, both countries can still benefit from trade. Even though the United States has an absolute advantage in producing both refrigerators and shoes, it makes economic sense for it to specialize in the good for which it has a comparative advantage. The United States will export refrigerators and in return import shoes.

6.3.3 How Opportunity Cost Sets the Boundaries of Trade

This example shows that both parties can benefit from specializing in their comparative advantages and trading. By using the opportunity costs in this example, it is possible to identify the range of possible trades that would benefit each country.

Mexico started out, before specialization and trade, producing 4,000 pairs of shoes and 5,000 refrigerators (see Figure and Table). Then, in the numerical example given, Mexico shifted production toward its comparative advantage and produced 6,000 pairs of shoes but only 2,500 refrigerators. Thus, if Mexico can export no more than 2,000 pairs of shoes (giving up 2,000 pairs of shoes) in exchange for imports of at least 2,500 refrigerators (a gain of 2,500 refrigerators), it will be able to consume more of both goods than before trade. Mexico will be unambiguously better off. Conversely, the United States started off, before specialization and trade, producing 5,000 pairs of shoes and 20,000 refrigerators. In the example, it then shifted production toward its comparative advantage, producing only 3,500 shoes but 26,000 refrigerators. If the United States can export no more than 6,000 refrigerators in exchange for imports of at least 1,500 pairs of shoes, it will be able to consume more of both goods and will be unambiguously better off.

The range of trades that can benefit both nations is shown in Table 6.11. For example, a trade where the U.S. exports 4,000 refrigerators to Mexico in exchange for 1,800 pairs of shoes would benefit both sides, in the sense that both countries would be able to consume more of both goods than in a world without trade.

The Range of Trades That Benefit Both the United States and Mexico

Table 6.11: The Range of Trades That Benefit Both the United States and Mexico

The U.S. economy, after specialization will benefit if it:

================================ Exports fewer than 6,000 refrigerators

The Mexican economy, after specialization will benefit if it:

================================ Imports at least 2,500 refrigerators

Imports at least 1,500 pairs of shoes

Exports no more than 2,000 pairs of shoes

Trade allows each country to take advantage of lower opportunity costs in the other country. If Mexico wants to produce more refrigerators without trade, it must face its domestic opportunity costs and reduce shoe production. If Mexico, instead, produces more shoes and then trades for refrigerators made in the United States, where the opportunity cost of producing refrigerators is lower, Mexico can in effect take advantage of the lower opportunity cost of refrigerators in the United States. Conversely, when the United States specializes in its comparative advantage of refrigerator production and trades for shoes produced in Mexico, international trade allows the United States to take advantage of the lower opportunity cost of shoe production in Mexico.

The theory of comparative advantage explains why countries trade: they have different comparative advantages. It shows that the gains from international trade result from pursuing comparative advantage and producing at a lower opportunity cost. The following Work It Out feature shows how to calculate absolute and comparative advantage and the way to apply them to a country’s production.

Note

CALCULATING ABSOLUTE AND COMPARATIVE ADVANTAGE

In Canada a worker can produce 20 barrels of oil or 40 tons of lumber. In Venezuela, a worker can produce 60 barrels of oil or 30 tons of lumber.

Table 6.12: 2 Country Example

Country

Oil (barrels)

Lumber (tons)

Canada

20 or

40

Venezuela

60 or

30

Who has the absolute advantage in the production of oil or lumber? How can you tell?

Which country has a comparative advantage in the production of oil?

Which country has a comparative advantage in producing lumber?

In this example, is absolute advantage the same as comparative advantage, or not?

In what product should Canada specialize? In what product should Venezuela specialize?

To calculate absolute advantage, look at the larger of the numbers for each product. One worker in Canada can produce more lumber (40 tons versus 30 tons), so Canada has the absolute advantage in lumber. One worker in Venezuela can produce 60 barrels of oil compared to a worker in Canada who can produce only 20.

Step 3.

To calculate comparative advantage, find the opportunity cost of producing one barrel of oil in both countries. The country with the lowest opportunity cost has the comparative advantage. With the same labor time, Canada can produce either 20 barrels of oil or 40 tons of lumber. So in effect, 20 barrels of oil is equivalent to 40 tons of lumber: 20 oil = 40 lumber. Divide both sides of the equation by 20 to calculate the opportunity cost of one barrel of oil in Canada. 20/20 oil = 40/20 lumber. 1 oil = 2 lumber. To produce one additional barrel of oil in Canada has an opportunity cost of 2 lumber. Calculate the same way for Venezuela: 60 oil = 30 lumber. Divide both sides of the equation by 60. One oil in Venezuela has an opportunity cost of 1/2 lumber. Because 1/2 lumber < 2 lumber, Venezuela has the comparative advantage in producing oil.

Step 4.

Calculate the opportunity cost of one lumber by reversing the numbers, with lumber on the left side of the equation. In Canada, 40 lumber is equivalent in labor time to 20 barrels of oil: 40 lumber = 20 oil. Divide each side of the equation by 40. The opportunity cost of one lumber is 1/2 oil. In Venezuela, the equivalent labor time will produce 30 lumber or 60 oil: 30 lumber = 60 oil. Divide each side by 30. One lumber has an opportunity cost of two oil. Canada has the lower opportunity cost in producing lumber.

Step 5.

In this example, absolute advantage is the same as comparative advantage. Canada has the absolute and comparative advantage in lumber; Venezuela has the absolute and comparative advantage in oil.

Step 6.

Canada should specialize in the commodity for which it has a relative lower opportunity cost, which is lumber, and Venezuela should specialize in oil. Canada will be exporting lumber and importing oil, and Venezuela will be exporting oil and importing lumber.

6.3.4 Terms of Trade and Consumption Possibilities Curve

The terms of trade (TOT) is the rate at which units of one product can be exchanged for units of another product. It is typically expressed as the price of the export good over the price of the import good:

The consumption possibilities curve shows the combinations of two goods that a nation can consume when it specializes in producing one good and trades with another nation.

6.3.5 Comparative Advantage Goes Camping

To build an intuitive understanding of how comparative advantage can benefit all parties, set aside examples that involve national economies for a moment and consider the situation of a group of friends who decide to go camping together. The six friends have a wide range of skills and experiences, but one person in particular, Jethro, has done lots of camping before and is also a great athlete. Jethro has an absolute advantage in all aspects of camping: he is faster at carrying a backpack, gathering firewood, paddling a canoe, setting up tents, making a meal, and washing up. So here is the question: Because Jethro has an absolute productivity advantage in everything, should he do all the work?

Of course not! Even if Jethro is willing to work like a mule while everyone else sits around, he, like all mortals, only has 24 hours in a day. If everyone sits around and waits for Jethro to do everything, not only will Jethro be an unhappy camper, but there will not be much output for his group of six friends to consume. The theory of comparative advantage suggests that everyone will benefit if they figure out their areas of comparative advantage—that is, the area of camping where their productivity disadvantage is least, compared to Jethro. For example, it may be that Jethro is 80% faster at building fires and cooking meals than anyone else, but only 20% faster at gathering firewood and 10% faster at setting up tents. In that case, Jethro should focus on building fires and making meals, and others should attend to the other tasks, each according to where their productivity disadvantage is smallest. If the campers coordinate their efforts according to comparative advantage, they can all gain.

Key Concepts and Summary

Even when a country has high levels of productivity in all goods, it can still benefit from trade.

Gains from trade come about as a result of comparative advantage.

By specializing in a good that it gives up the least to produce, a country can produce more and offer that additional output for sale.

If other countries specialize in the area of their comparative advantage as well and trade, the highly productive country is able to benefit from a lower opportunity cost of production in other countries.

Self-Check Questions

Is it possible to have a comparative advantage in the production of a good but not to have an absolute advantage? Explain.

How does comparative advantage lead to gains from trade?

You just overheard your friend say the following: “Poor countries like Malawi have no absolute advantages. They have poor soil, low investments in formal education and hence low-skill workers, no capital, and no natural resources to speak of. Because they have no advantage, they cannot benefit from trade.” How would you respond?

You just got a job in Washington, D.C. You move into an apartment with some acquaintances. All your roommates, however, are slackers and do not clean up after themselves. You, on the other hand, can clean faster than each of them. You determine that you are 70% faster at dishes and 10% faster with vacuuming. All of these tasks have to be done daily. Which jobs should you assign to your roommates to get the most free time overall? Assume you have the same number of hours to devote to cleaning. Now, since you are faster, you seem to get done quicker than your roommate. What sorts of problems may this create? Can you imagine a trade-related analogy to this problem?

6.4 Intra-industry Trade between Similar Economies

Chapter Learning Objectives

Identify at least two advantages of intra-industry trading

Explain the relationship between economies of scale and intra-industry trade

Absolute and comparative advantages explain a great deal about global trading patterns. For example, they help to explain the patterns that we noted at the start of this chapter, like why you may be eating fresh fruit from Chile or Mexico, or why lower productivity regions like Africa and Latin America are able to sell a substantial proportion of their exports to higher productivity regions like the European Union and North America. Comparative advantage, however, at least at first glance, does not seem especially well-suited to explain other common patterns of international trade.

6.4.1 The Prevalence of Intra-industry Trade between Similar Economies

The theory of comparative advantage suggests that trade should happen between economies with large differences in opportunity costs of production. Roughly half of all world trade involves shipping goods between the fairly similar high-income economies of the United States, Canada, the European Union, Japan, Mexico, and China (see Table 6.13).

Moreover, the theory of comparative advantage suggests that each economy should specialize to a degree in certain products, and then exchange those products. A high proportion of trade, however, is intra-industry trade—that is, trade of goods within the same industry from one country to another. For example, the United States produces and exports autos and imports autos.

Table 6.14 shows some of the largest categories of U.S. exports and imports. In all of these categories, the United States is both a substantial exporter and a substantial importer of goods from the same industry. In 2014, according to the Bureau of Economic Analysis, the United States exported $146 billion worth of autos, and imported $327 billion worth of autos. About 60% of U.S. trade and 60% of European trade is intra-industry trade.

Why do similar high-income economies engage in intra-industry trade? What can be the economic benefit of having workers of fairly similar skills making cars, computers, machinery and other products which are then shipped across the oceans to and from the United States, the European Union, and Japan? There are two reasons: (1) The division of labor leads to learning, innovation, and unique skills; and (2) economies of scale.

6.4.2 Gains from Specialization and Learning

Consider the category of machinery, where the U.S. economy has considerable intra-industry trade. Machinery comes in many varieties, so the United States may be exporting machinery for manufacturing with wood, but importing machinery for photographic processing. The underlying reason why a country like the United States, Japan, or Germany produces one kind of machinery rather than another is usually not related to U.S., German, or Japanese firms and workers having generally higher or lower skills. It is just that, in working on very specific and particular products, firms in certain countries develop unique and different skills.

Specialization in the world economy can be very finely split. In fact, recent years have seen a trend in international trade, which economists call splitting up the value chain. The value chain describes how a good is produced in stages. As indicated in the beginning of the chapter, producing the iPhone involves designing and engineering the phone in the United States, supplying parts from Korea, assembling the parts in China, and advertising and marketing in the United States. Thanks in large part to improvements in communication technology, sharing information, and transportation, it has become easier to split up the value chain. Instead of production in a single large factory, different firms operating in various places and even different countries can divide the value chain. Because firms split up the value chain, international trade often does not involve nations trading whole finished products like automobiles or refrigerators. Instead, it involves shipping more specialized goods like, say, automobile dashboards or the shelving that fits inside refrigerators. Intra-industry trade between similar countries produces economic gains because it allows workers and firms to learn and innovate on particular products—and often to focus on very particular parts of the value chain.

6.4.3 Economies of Scale, Competition, Variety

A second broad reason that intra-industry trade between similar nations produces economic gains involves economies of scale. The concept of economies of scale, as we introduced in Production, Costs and Industry Structure, means that as the scale of output goes up, average costs of production decline—at least up to a point.

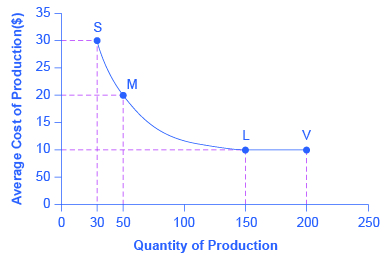

Figure 6.5 illustrates economies of scale for a plant producing toaster ovens. The horizontal axis of the figure shows the quantity of production by a certain firm or at a certain manufacturing plant. The vertical axis measures the average cost of production. Production plant S produces a small level of output at 30 units and has an average cost of production of $30 per toaster oven. Plant M produces at a medium level of output at 50 units, and has an average cost of production of $20 per toaster oven. Plant L produces 150 units of output with an average cost of production of only $10 per toaster oven. Although plant V can produce 200 units of output, it still has the same unit cost as Plant L.

In this example, a small or medium plant, like S or M, will not be able to compete in the market with a large or a very large plant like L or V, because the firm that operates L or V will be able to produce and sell its output at a lower price. In this example, economies of scale operate up to point L, but beyond point L to V, the additional scale of production does not continue to reduce average costs of production.

Figure 6.5: Economies of Scale. Production Plant S, has an average cost of production of $30 per toaster oven. Production plant M has an average cost of production of $20 per toaster oven. Production plant L has an average cost of production of only $10 per toaster oven. Production plant V still has an average cost of production of $10 per toaster oven. Thus, production plant M can produce toaster ovens more cheaply than plant S because of economies of scale, and plants L or V can produce more cheaply than S or M because of economies of scale. However, the economies of scale end at an output level of 150. Plant V, despite being larger, cannot produce more cheaply on average than plant L.

The graph shows declining average costs. The x-axis plots the quantity of production or the scale of the plant and the y-axis plots the average costs. The average cost curve is a declining function, starting at (30, 30) with plant S, declining at a decreasing rate to (150, 10) with plant L, and (200, 10) with plant V, as explained in the text.

The concept of economies of scale becomes especially relevant to international trade when it enables one or two large producers to supply the entire country. For example, a single large automobile factory could probably supply all the cars consumers purchase in a smaller economy like the United Kingdom or Belgium in a given year. However, if a country has only one or two large factories producing cars, and no international trade, then consumers in that country would have relatively little choice between kinds of cars (other than the color of the paint and other nonessential options). Little or no competition will exist between different car manufacturers.

International trade provides a way to combine the lower average production costs that come from economies of scale and still have competition and variety for consumers. Large automobile factories in different countries can make and sell their products around the world. If General Motors, Ford, and Chrysler were the only players in the U.S. automobile market, the level of competition and consumer choice would be considerably lower than when U.S. carmakers must face competition from Toyota, Honda, Suzuki, Fiat, Mitsubishi, Nissan, Volkswagen, Kia, Hyundai, BMW, Subaru, and others. Greater competition brings with it innovation and responsiveness to what consumers want. America’s car producers make far better cars now than they did several decades ago, and much of the reason is competitive pressure, especially from East Asian and European carmakers.

6.4.4 Dynamic Comparative Advantage

The sources of gains from intra-industry trade between similar economies—namely, the learning that comes from a high degree of specialization and splitting up the value chain and from economies of scale—do not contradict the earlier theory of comparative advantage. Instead, they help to broaden the concept.

In intra-industry trade, climate or geography do not determine the level of worker productivity. Even the general level of education or skill does not determine it. Instead, how firms engage in specific learning about specialized products, including taking advantage of economies of scale determine the level of worker productivity. In this vision, comparative advantage can be dynamic—that is, it can evolve and change over time as one develops new skills and as manufacturers split the value chain in new ways. This line of thinking also suggests that countries are not destined to have the same comparative advantage forever, but must instead be flexible in response to ongoing changes in comparative advantage.

Key Concepts and Summary

A large share of global trade happens between high-income economies that are quite similar in having well-educated workers and advanced technology.

These countries practice intra-industry trade, in which they import and export the same products at the same time, like cars, machinery, and computers.

In the case of intra-industry trade between economies with similar income levels, the gains from trade come from specialized learning in very particular tasks and from economies of scale.

Splitting up the value chain means that several stages of producing a good take place in different countries around the world.

Self-Check Questions

What is intra-industry trade?

What are the two main sources of economic gains from intra-industry trade?

What is splitting up the value chain?

Does intra-industry trade contradict the theory of comparative advantage?

Do consumers benefit from intra-industry trade?

Why might intra-industry trade seem surprising from the point of view of comparative advantage?

6.5 The Benefits of Reducing Barriers to International Trade

Chapter Learning Objectives

Explain tarrifs as barriers to trade

Identify at least two benefits of reducing barriers to international trade

Tariffs are taxes that governments place on imported goods for a variety of reasons. Some of these reasons include protecting sensitive industries, for humanitarian reasons, and protecting against dumping. Traditionally, tariffs were used simply as a political tool to protect certain vested economic, social, and cultural interests. The World Trade Organization (WTO) is committed to lowering barriers to trade. The world’s nations meet through the WTO to negotiate how they can reduce barriers to trade, such as tariffs. WTO negotiations happen in “rounds,” where all countries negotiate one agreement to encourage trade, take a year or two off, and then start negotiating a new agreement. The current round of negotiations is called the Doha Round because it was officially launched in Doha, the capital city of Qatar, in November 2001. In 2009, economists from the World Bank summarized recent research and found that the Doha round of negotiations would increase the size of the world economy by $160 billion to $385 billion per year, depending on the precise deal that ended up being negotiated.

In the context of a global economy that currently produces more than $30 trillion of goods and services each year, this amount is not huge: it is an increase of 1% or less. But before dismissing the gains from trade too quickly, it is worth remembering two points.

First, a gain of a few hundred billion dollars is enough money to deserve attention! Moreover, remember that this increase is not a one-time event; it would persist each year into the future.

Second, the estimate of gains may be on the low side because some of the gains from trade are not measured especially well in economic statistics. For example, it is difficult to measure the potential advantages to consumers of having a variety of products available and a greater degree of competition among producers. Perhaps the most important unmeasured factor is that trade between countries, especially when firms are splitting up the value chain of production, often involves a transfer of knowledge that can involve skills in production, technology, management, finance, and law.

Low-income countries benefit more from trade than high-income countries do. In some ways, the giant U.S. economy has less need for international trade, because it can already take advantage of internal trade within its economy. However, many smaller national economies around the world, in regions like Latin America, Africa, the Middle East, and Asia, have much more limited possibilities for trade inside their countries or their immediate regions. Without international trade, they may have little ability to benefit from comparative advantage, slicing up the value chain, or economies of scale. Moreover, smaller economies often have fewer competitive firms making goods within their economy, and thus firms have less pressure from other firms to provide the goods and prices that consumers want.

The economic gains from expanding international trade are measured in hundreds of billions of dollars, and the gains from international trade as a whole probably reach well into the trillions of dollars. The potential for gains from trade may be especially high among the smaller and lower-income countries of the world.

6.5.1 From Interpersonal to International Trade

Most people find it easy to believe that they, personally, would not be better off if they tried to grow and process all of their own food, to make all of their own clothes, to build their own cars and houses from scratch, and so on. Instead, we all benefit from living in economies where people and firms can specialize and trade with each other.

The benefits of trade do not stop at national boundaries, either. Earlier we explained that the division of labor could increase output for three reasons: (1) workers with different characteristics can specialize in the types of production where they have a comparative advantage; (2) firms and workers who specialize in a certain product become more productive with learning and practice; and (3) economies of scale. These three reasons apply from the individual and community level right up to the international level. If it makes sense to you that interpersonal, intercommunity, and interstate trade offer economic gains, it should make sense that international trade offers gains, too.

International trade currently involves about $20 trillion worth of goods and services moving around the globe. Any economic force of that size, even if it confers overall benefits, is certain to cause disruption and controversy. This chapter has only made the case that trade brings economic benefits. Other chapters discuss, in detail, the public policy arguments over whether to restrict international trade.

Note

IT’S APPLE’S (GLOBAL) IPHONE

Apple Corporation uses a global platform to produce the iPhone. Now that you understand the concept of comparative advantage, you can see why the engineering and design of the iPhone is done in the United States. The United States has built up a comparative advantage over the years in designing and marketing products, and sacrifices fewer resources to design high-tech devices relative to other countries.

China has a comparative advantage in assembling the phone due to its large skilled labor force. Korea has a comparative advantage in producing components. Korea focuses its production by increasing its scale, learning better ways to produce screens and computer chips, and uses innovation to lower average costs of production. Apple, in turn, benefits because it can purchase these quality products at lower prices. Put the global assembly line together and you have the device with which we are all so familiar.

Key Concepts and Summary

Tariffs are placed on imported goods as a way of protecting sensitive industries, for humanitarian reasons, and for protection against dumping.

Traditionally, tariffs were used as a political tool to protect certain vested economic, social, and cultural interests.

The WTO has been, and continues to be, a way for nations to meet and negotiate in order to reduce barriers to trade.

The gains of international trade are very large, especially for smaller countries, but are beneficial to all.

Self-Check Questions

If the removal of trade barriers is so beneficial to international economic growth, why would a nation continue to restrict trade on some imported or exported products?

Are the gains from international trade more likely to be relatively more important to large or small countries?

In World Trade Organization meetings, what do you think low-income countries lobby for?

Why might a low-income country put up barriers to trade, such as tariffs on imports?

Can a nation’s comparative advantage change over time? What factors would make it change?

6.6 Measuring Trade Balances

Chapter Learning Objectives

Measuring Trade Balances

Trade Balances in Historical and International Context

Trade Balances and Flows of Financial Capital

The National Saving and Investment Identity

The Pros and Cons of Trade Deficits and Surpluses

The Difference between Level of Trade and the Trade Balance

Explain merchandise trade balance, current account balance, and unilateral transfers

Identify components of the U.S. current account balance

Calculate the merchandise trade balance and current account balance using import and export data for a country

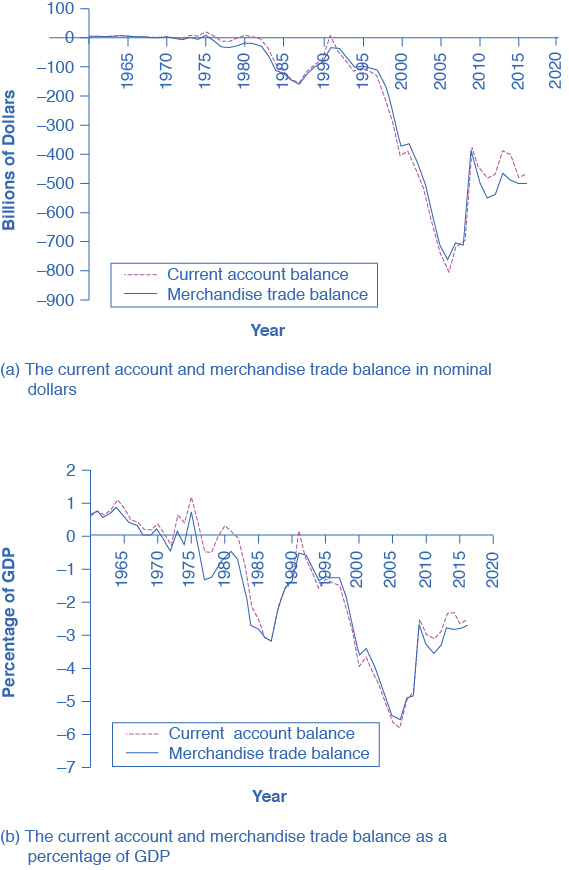

The balance of trade (or trade balance) is any gap between a nation’s dollar value of its exports, or what its producers sell abroad, and a nation’s dollar value of imports, or the foreign-made products and services that households and businesses purchase. Recall from The Macroeconomic Perspective that if exports exceed imports, the economy has a trade surplus. If imports exceed exports, the economy has a trade deficit. If exports and imports are equal, then trade is balanced, but what happens when trade is out of balance and large trade surpluses or deficits exist?

Germany, for example, has had substantial trade surpluses in recent decades, in which exports have greatly exceeded imports. According to the Central Intelligence Agency’s The World Factbook, in 2016, Germany ran a trade surplus of $295 billion. In contrast, the U.S. economy in recent decades has experienced large trade deficits, in which imports have considerably exceeded exports. In 2016, for example, U.S. imports exceeded exports by $502 billion.

A series of financial crises triggered by unbalanced trade can lead economies into deep recessions. These crises begin with large trade deficits. At some point, foreign investors become pessimistic about the economy and move their money to other countries. The economy then drops into deep recession, with real GDP often falling up to 10% or more in a single year. This happened to Mexico in 1995 when their GDP fell 8.1%. A number of countries in East Asia—Thailand, South Korea, Malaysia, and Indonesia—succumbed to the same economic illness in 1997–1998 (called the Asian Financial Crisis). In the late 1990s and into the early 2000s, Russia and Argentina had the identical experience. What are the connections between imbalances of trade in goods and services and the flows of international financial capital that set off these economic avalanches?

We will start by examining the balance of trade in more detail, by looking at some patterns of trade balances in the United States and around the world. Then we will examine the intimate connection between international flows of goods and services and international flows of financial capital, which to economists are really just two sides of the same coin. People often assume that trade surpluses like those in Germany must be a positive sign for an economy, while trade deficits like those in the United States must be harmful. As it turns out, both trade surpluses and deficits can be either good or bad. We will see why in this chapter.

Figure 6.6: We are all part of the global financial system, which includes many different currencies. (Credit: modification of work by epSos.de/Flickr Creative Commons)

Note

MORE THAN MEETS THE EYE IN THE CONGO

How much do you interact with the global financial system? Do you think not much? Think again. Suppose you take out a student loan, or you deposit money into your bank account. You just affected domestic savings and borrowing. Now say you are at the mall and buy two T-shirts “made in China,” and later contribute to a charity that helps refugees. What is the impact? You affected how much money flows into and out of the United States. If you open an IRA savings account and put money in an international mutual fund, you are involved in the flow of money overseas. While your involvement may not seem as influential as that of someone like the president, who can increase or decrease foreign aid and, thereby, have a huge impact on money flows in and out of the country, you do interact with the global financial system on a daily basis.

The balance of payments—a term you will meet soon—seems like a huge topic, but once you learn the specific components of trade and money, it all makes sense. Along the way, you may have to give up some common misunderstandings about trade and answer some questions: If a country is running a trade deficit, is that bad? Is a trade surplus good? For example, look at the Democratic Republic of the Congo (often referred to as “Congo”), a large country in Central Africa. In 2013, it ran a trade surplus of $1 billion, so it must be doing well, right? In contrast, the trade deficit in the United States was $508 billion in 2013. Do these figures suggest that the United States economy is performing worse than the Congolese economy? Not necessarily. The U.S. trade deficit tends to worsen as the economy strengthens. In contrast, high poverty rates in the Congo persist, and these rates are not going down even with the positive trade balance. Clearly, it is more complicated than simply asserting that running a trade deficit is bad for the economy. You will learn more about these issues and others in this chapter.

A few decades ago, it was common to track the solid or physical items that planes, trains, and trucks transported between countries as a way of measuring the balance of trade. Economists call this measurement is called the merchandise trade balance. In most high-income economies, including the United States, goods comprise less than half of a country’s total production, while services comprise more than half. The last two decades have seen a surge in international trade in services, powered by technological advances in telecommunications and computers that have made it possible to export or import customer services, finance, law, advertising, management consulting, software, construction engineering, and product design. Most global trade still takes the form of goods rather than services, and the government announces and the media prominently report the merchandise trade balance. Old habits are hard to break. Economists, however, typically rely on broader measures such as the balance of trade or the current account balance which includes other international flows of income and foreign aid.

6.6.1 Components of the U.S. Current Account Balance

Table 6.15 breaks down the four main components of the U.S. current account balance for the last quarter of 2015 (seasonally adjusted). The first line shows the merchandise trade balance; that is, exports and imports of goods. Because imports exceed exports, the trade balance in the final column is negative, showing a merchandise trade deficit. We can explain how the government collects this trade information in the following Clear It Up feature.

Table 6.15: Components of the U.S. Current Account Balance for 2015 (in billions)

Value of Exports (money

| flowing into U.S.)

Value of Imports (money

| flowing out of U.S.)

Ba lance

Goods

$410.0

$595.5

–$ 185.3

Services

$180.4

$122.3

$58.1

Income receipts

and payments

$203.0

$152.4

$50.6

Unilateral

transfers

$27.3

$64.4

–

$37.1

Current account

balance

$820.7

$934.4

–$ 113.7

Note

HOW DOES THE U.S. GOVERNMENT COLLECT TRADE STATISTICS?

Do not confuse the balance of trade (which tracks imports and exports), with the current account balance, which includes not just exports and imports, but also income from investment and transfers.

The Bureau of Economic Analysis (BEA) within the U.S. Department of Commerce compiles statistics on the balance of trade using a variety of different sources. Merchandise importers and exporters must file monthly documents with the Census Bureau, which provides the basic data for tracking trade. To measure international trade in services—which can happen over a telephone line or computer network without shipping any physical goods—the BEA carries out a set of surveys. Another set of BEA surveys tracks investment flows, and there are even specific surveys to collect travel information from U.S. residents visiting Canada and Mexico. For measuring unilateral transfers, the BEA has access to official U.S. government spending on aid, and then also carries out a survey of charitable organizations that make foreign donations.

The BEA then cross-checks this information on international flows of goods and capital against other available data. For example, the Census Bureau also collects data from the shipping industry, which it can use to check the data on trade in goods. All companies involved in international flows of capital—including banks and companies making financial investments like stocks—must file reports, which the U.S. Department of the Treasury ultimately checks. The BEA also can cross check information on foreign trade by looking at data collected by other countries on their foreign trade with the United States, and also at the data collected by various international organizations. Take these data sources, stir carefully, and you have the U.S. balance of trade statistics. Much of the statistics that we cite in this chapter come from these sources.

The second row of Table 6.15 provides data on trade in services. Here, the U.S. economy is running a surplus. Although the level of trade in services is still relatively small compared to trade in goods, the importance of services has expanded substantially over the last few decades. For example, U.S. exports of services were equal to about one-half of U.S. exports of goods in 2015, compared to one-fifth in 1980.

The third component of the current account balance, labeled “income payments,” refers to money that U.S. financial investors received on their foreign investments (money flowing into the United States) and payments to foreign investors who had invested their funds here (money flowing out of the United States). The reason for including this money on foreign investment in the overall measure of trade, along with goods and services, is that, from an economic perspective, income is just as much an economic transaction as car, wheat, or oil shipments: it is just trade that is happening in the financial capital market.

The final category of the current account balance is unilateral transfers, which are payments that government, private charities, or individuals make in which they send money abroad without receiving any direct good or service. Economic or military assistance from the U.S. government to other countries fits into this category, as does spending abroad by charities to address poverty or social inequalities. When an individual in the United States sends money overseas, as is the case with some immigrants, it is also counted in this category. The current account balance treats these unilateral payments like imports, because they also involve a stream of payments leaving the country. For the U.S. economy, unilateral transfers are almost always negative. This pattern, however, does not always hold. In 1991, for example, when the United States led an international coalition against Saddam Hussein’s Iraq in the Gulf War, many other nations agreed that they would make payments to the United States to offset the U.S. war expenses. These payments were large enough that, in 1991, the overall U.S. balance on unilateral transfers was a positive $10 billion.

The following Work It Out feature steps you through the process of using the values for goods, services, and income payments to calculate the merchandise balance and the current account balance.

Note

CALCULATING THE MERCHANDISE BALANCE AND THE CURRENT ACCOUNT BALANCE

Table 6.16: Calculating Merchandise Balance and Current Account Balance

Item

Exports (in $ billions)

Imports (in $ billions)

Balance

Goods Services Income payments Unilateral transfers Current account balance

Use the information given below to fill in Table 6.16, and then calculate:

The merchandise balance

The current account balance

Known information:

Unilateral transfers: $130

Exports in goods: $1,046

Exports in services: $509

Imports in goods: $1,562

Imports in services: $371

Income received by U.S. investors on foreign stocks and bonds: $561

Income received by foreign investors on U.S. assets: $472

Step 1.

Focus on goods and services first. Enter the dollar amount of exports of both goods and services under the Export column.

Step 2.

Enter imports of goods and services under the Import column.

Step 3.

Under the Export column and in the row for Income payments, enter the financial flows of money coming back to the United States. U.S. investors are earning this income from abroad.

Step 4.

Under the Import column and in the row for Income payments, enter the financial flows of money going out of the United States to foreign investors. Foreign investors are earning this money on U.S. assets, like stocks.

Step 5.

Unilateral transfers are money flowing out of the United States in the form of, for example, military aid, foreign aid, and global charities. Because the money leaves the country, enter it under Imports and in the final column as well, as a negative.

Step 6.

Calculate the trade balance by subtracting imports from exports in both goods and services. Enter this in the final Balance column. This can be positive or negative.

Step 7.

Subtract the income payments flowing out of the country (under Imports) from the money coming back to the United States (under Exports) and enter this amount under the Balance column.

Step 8.

Enter unilateral transfers as a negative amount under the Balance column.

Step 9.

The merchandise trade balance is the difference between exports of goods and imports of goods—the first number under Balance.

Step 10.

Now sum up your columns for Exports, Imports, and Balance. The final balance number is the current account balance.

The merchandise balance of trade is the difference between exports and imports. In this case, it is equal to $1,046 – $1,562, a trade deficit of –$516 billion. The current account balance is –$419 billion. See the completed Table 6.17.

Table 6.17: Completed Merchandise Balance and Current Account Balance

Value of Exports (money flowing into U.S.)

Value of Imports (money flowing out of U.S.)

Ba lance

Goods

$1,510.3

$2,272.9

–$ 762.6

Services

$750.9

$488.7

$ 262.2

Income receipts

and payments

$782.9

$600.5

$ 182.4

Unilateral

transfers

$128.6

$273.6

–$ 145.0

Current account

balance

$3,172.7

$3,635.7

–$ 463.0

Key Concepts and Summary

The trade balance measures the gap between a country’s exports and its imports.

In most high-income economies, goods comprise less than half of a country’s total production, while services comprise more than half.

The last two decades have seen a surge in international trade in services; however, most global trade still takes the form of goods rather than services.

The current account balance includes the trade in goods, services, and money flowing into and out of a country from investments and unilateral transfers.

Self-Check Questions

If foreign investors buy more U.S. stocks and bonds, how would that show up in the current account balance?

If the trade deficit of the United States increases, how is the current account balance affected?

State whether each of the following events involves a financial flow to the Mexican economy or a financial flow out of the Mexican economy:

: a. Mexico imports services from Japan b. Mexico exports goods to Canada c. U.S. investors receive a return from past financial investments in Mexico

If imports exceed exports, is it a trade deficit or a trade surplus? What about if exports exceed imports?

What is included in the current account balance?

Occasionally, a government official will argue that a country should strive for both a trade surplus and a healthy inflow of capital from abroad. Explain why such a statement is economically impossible.

A government official announces a new policy. The country wishes to eliminate its trade deficit, but will strongly encourage financial investment from foreign firms. Explain why such a statement is contradictory.

6.7 Trade Balances in Historical and International Context

Chapter Learning Objectives

Analyze graphs of the current account balance and the merchandise trade balance

Identify patterns in U.S. trade surpluses and deficits

Compare the U.S. trade surpluses and deficits to other countries' trade surpluses and deficits

Code

import osimport numpy as npimport pandas as pdimport matplotlib.pyplot as pltimport seaborn as snstitleSize =16sns.set_style("whitegrid", {'grid.linestyle': ':'})max_year =2026# max year in time series graphs# -----------------------------------------------------------------------------## Load datadf_a = pd.read_csv('Graphs/Annual_FRED.csv', header=0, index_col=0, parse_dates=True)df_q = pd.read_csv('Graphs/Quarterly_FRED.csv', header=0, index_col=0, parse_dates=True)df_m = pd.read_csv('Graphs/Monthly_FRED.csv', header=0, index_col=0, parse_dates=True)# -----------------------------------------------------------------------------df_q['ExportsTrill'] = df_q['Exports']/1000df_q['ImportsTrill'] = df_q['Imports']/1000df_q['GDPTrill'] = df_q['GDP']/1000df_q['GNPTrill'] = df_q['GNP']/1000df_q['realGDPTrill'] = df_q['rGDP']/1000df_q['ExportsGDP'] = df_q['Exports']/df_q['GDP']*100df_q['ImportsGDP'] = df_q['Imports']/df_q['GDP']*100df_q['TradeBalance'] = (df_q['Exports']-df_q['Imports'])/df_q['GDP']*100

Code

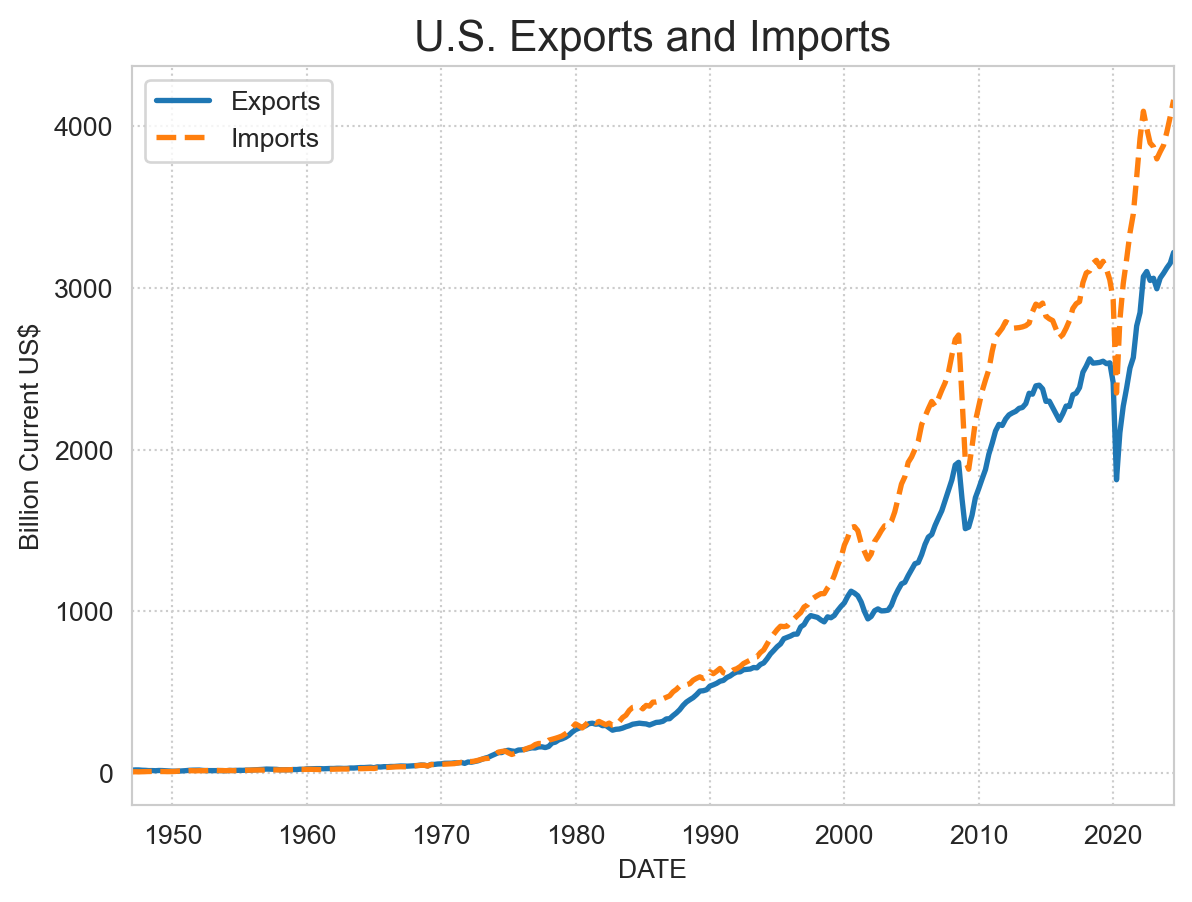

df_q[['Exports', 'Imports']].plot(style = ['-', '--'], linewidth=2)plt.title('U.S. Exports and Imports', fontsize=titleSize)plt.ylabel('Billion Current US$')plt.show()

Figure 6.7: US exports and imports in billion USD

Code

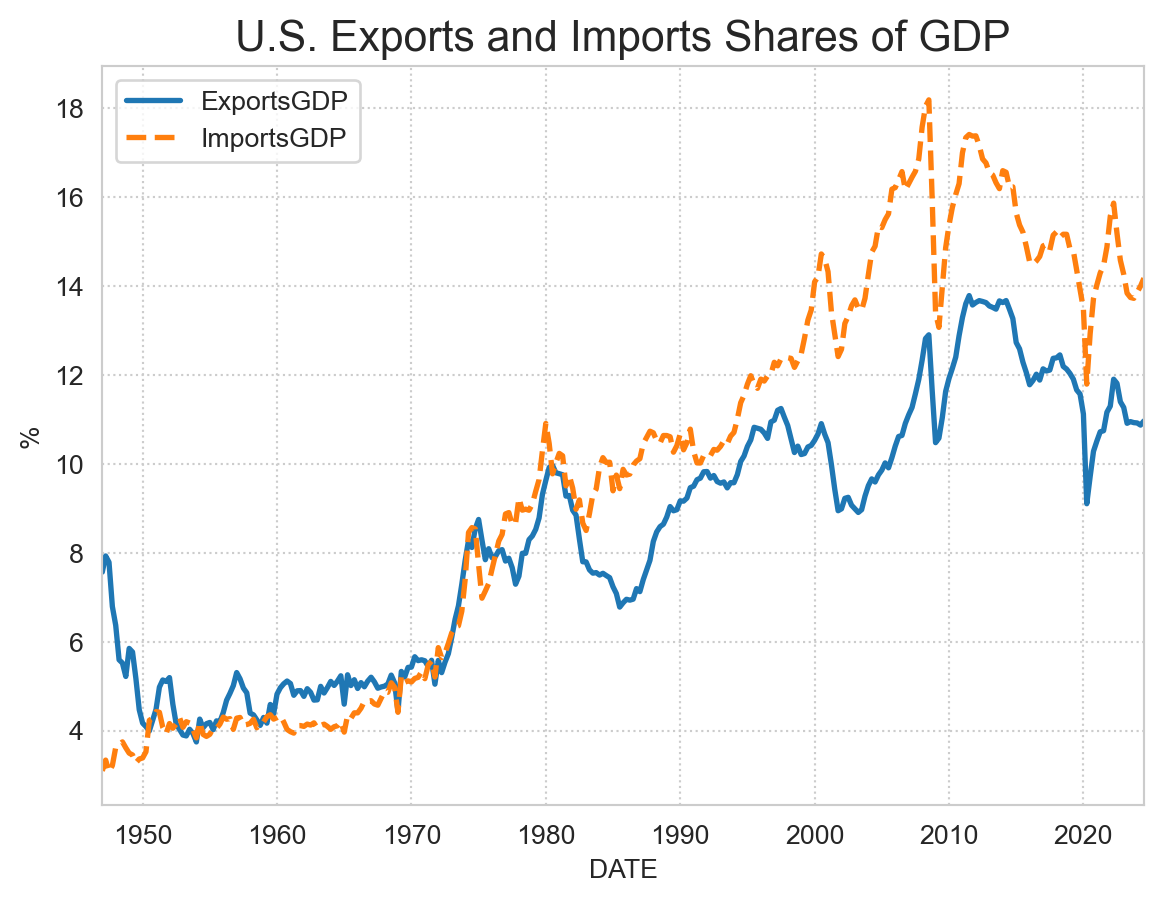

df_q[['ExportsGDP', 'ImportsGDP']].plot(style = ['-', '--'], linewidth=2)plt.title('U.S. Exports and Imports Shares of GDP', fontsize=titleSize)plt.ylabel('%')plt.show()

Figure 6.8: US exports and imports as percent of GDP

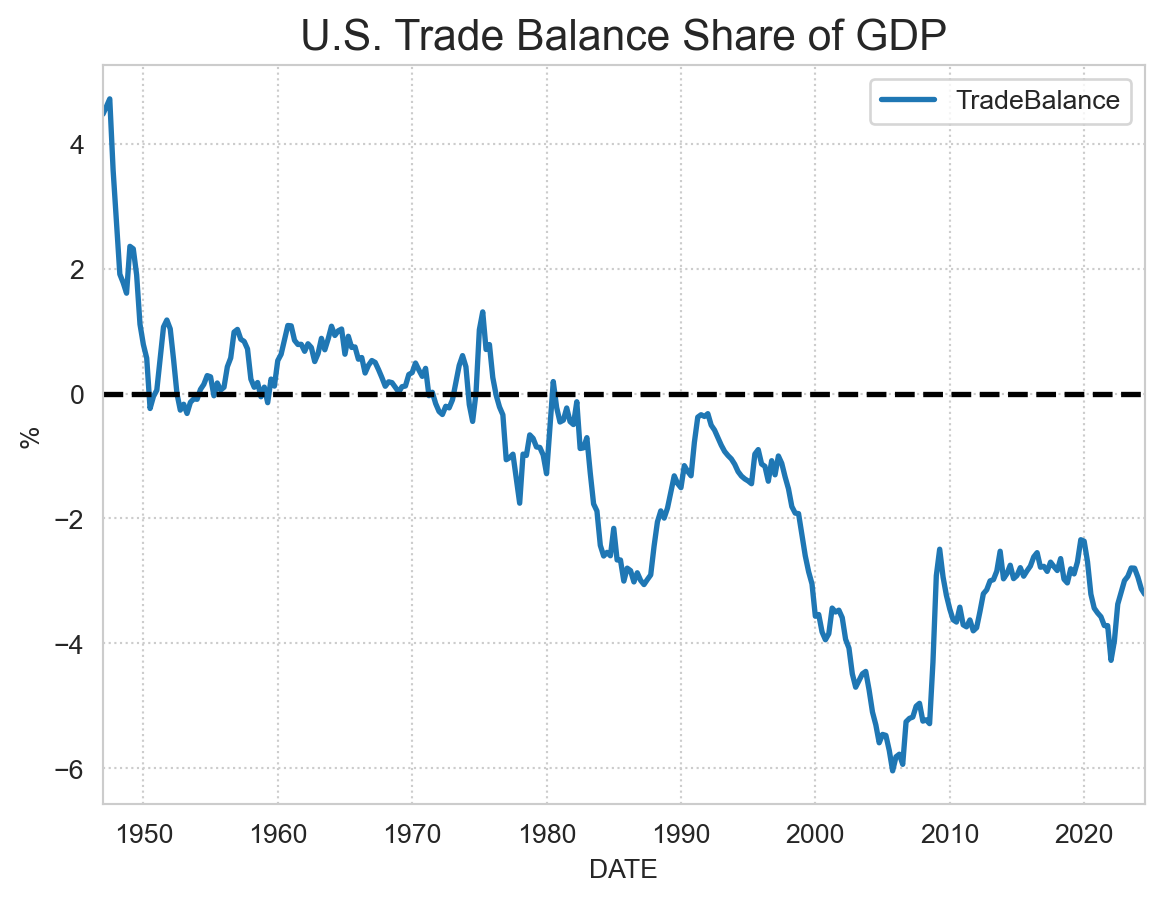

Figure 6.9: US trade balance is Exports minus Imports as share of GDP

Code

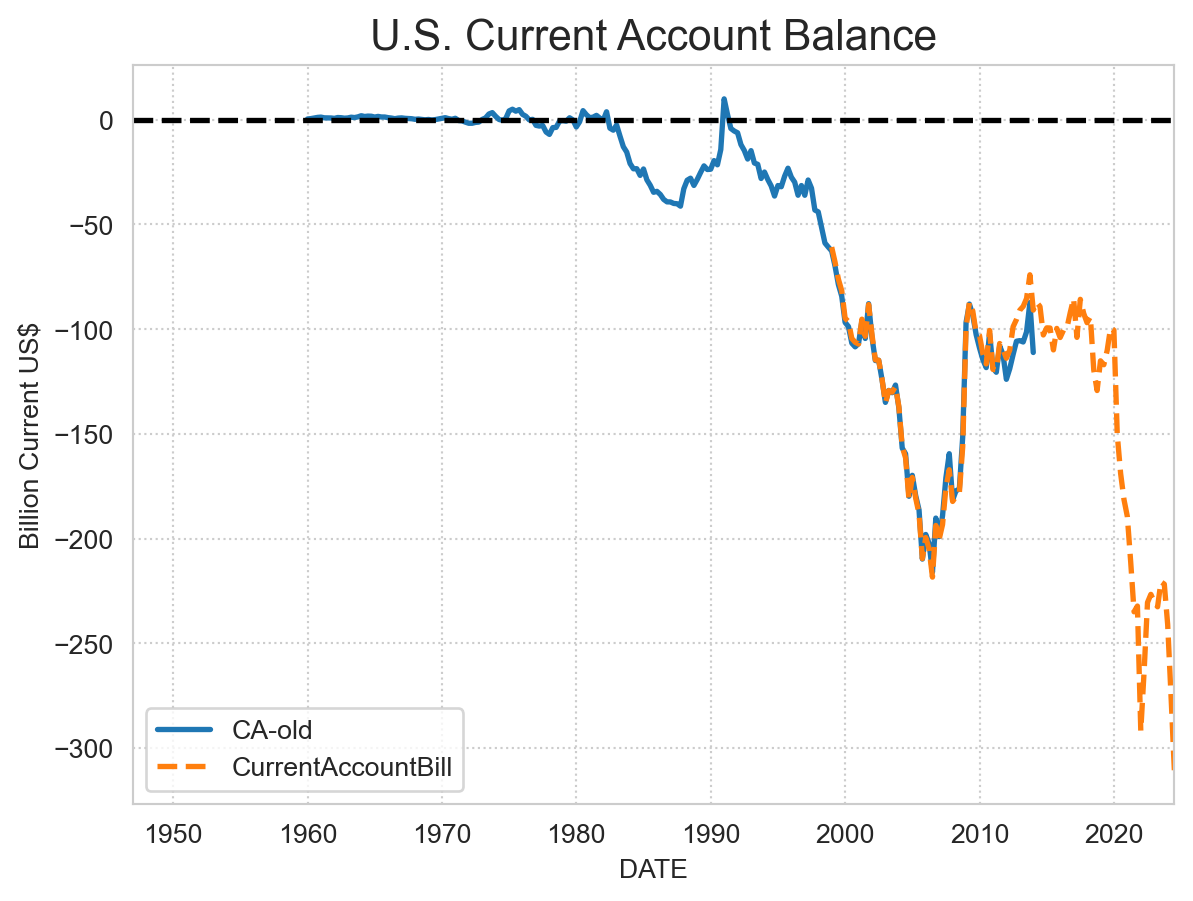

df_q['CurrentAccountBill'] = df_q['CurrentAccount']/1000(df_q[['CA-old', 'CurrentAccountBill']]).plot(style = ['-','--'], linewidth=2)plt.title('U.S. Current Account Balance', fontsize=titleSize)plt.axhline(y=0, xmin=0, xmax = max_year, linewidth=2, linestyle='--', color='black')plt.ylabel('Billion Current US$')plt.show()

Figure 6.10: Current account balance

In Figure 6.7 we show the time series plots of US exports and imports in billions of current US dollars.

In Figure 6.8 we show exports and imports as fraction of GDP. In Figure 6.9 we show the trade balance as percent of GDP. The trade balance is the difference between exports and imports. Finally, in Figure 6.10 we show the current account balance in billions of USD.