11 Aggregate Demand and Aggregate Supply

A key part of macroeconomics is the use of models to analyze macro issues and problems. How is the rate of economic growth connected to changes in the unemployment rate? Is there a reason why unemployment and inflation seem to move in opposite directions: lower unemployment and higher inflation from 1997 to 2000, higher unemployment and lower inflation in the early 2000s, lower unemployment and higher inflation in the mid-2000s, and then higher unemployment and lower inflation in 2009? Why did the current account deficit rise so high, but then decline in 2009?

To analyze questions like these, we must move beyond discussing macroeconomic issues one at a time, and begin building economic models that will capture the relationships and interconnections between them. The next three chapters take up this task. This chapter introduces the macroeconomic model of aggregate supply and aggregate demand, how the two interact to reach a macroeconomic equilibrium, and how shifts in aggregate demand or aggregate supply will affect that equilibrium. This chapter also relates the model of aggregate supply and aggregate demand to the three goals of economic policy (growth, unemployment, and inflation), and provides a framework for thinking about many of the connections and tradeoffs between these goals. The chapter on The Keynesian Perspective focuses on the macroeconomy in the short run, where aggregate demand plays a crucial role. The chapter on The Neoclassical Perspective explores the macroeconomy in the long run, where aggregate supply plays a crucial role.

11.1 Macroeconomic Perspectives on Demand and Supply

Macroeconomists over the last two centuries have often divided into two groups: those who argue that supply is the most important determinant of the size of the macroeconomy while demand just tags along, and those who argue that demand is the most important factor in the size of the macroeconomy while supply just tags along.

11.1.1 Say’s Law and the Macroeconomics of Supply

Those economists who emphasize the role of supply in the macroeconomy often refer to the work of a famous French economist of the early nineteenth century named Jean-Baptiste Say (1767–1832). Say’s law is: “Supply creates its own demand.” As a matter of historical accuracy, it seems clear that Say never actually wrote down this law and that it oversimplifies his beliefs, but the law lives on as useful shorthand for summarizing a point of view.

The intuition behind Say’s law is that each time a good or service is produced and sold, it generates income that is earned for someone: a worker, a manager, an owner, or those who are workers, managers, and owners at firms that supply inputs along the chain of production. The forces of supply and demand in individual markets will cause prices to rise and fall. The bottom line remains, however, that every sale represents income to someone, and so, Say’s law argues, a given value of supply must create an equivalent value of demand somewhere else in the economy. Because Jean-Baptiste Say, Adam Smith, and other economists writing around the turn of the nineteenth century who discussed this view were known as “classical” economists, modern economists who generally subscribe to the Say’s law view on the importance of supply for determining the size of the macroeconomy are called neoclassical economists.

If supply always creates exactly enough demand at the macroeconomic level, then (as Say himself recognized) it is hard to understand why periods of recession and high unemployment should ever occur. To be sure, even if total supply always creates an equal amount of total demand, the economy could still experience a situation of some firms earning profits while other firms suffer losses. Nevertheless, a recession is not a situation where all business failures are exactly counterbalanced by an offsetting number of successes. A recession is a situation in which the economy as a whole is shrinking in size, business failures outnumber the remaining success stories, and many firms end up suffering losses and laying off workers.

Say’s law that supply creates its own demand does seem a good approximation for the long run. Over periods of some years or decades, as the productive power of an economy to supply goods and services increases, total demand in the economy grows at roughly the same pace. However, over shorter time horizons of a few months or even years, recessions or even depressions occur in which firms, as a group, seem to face a lack of demand for their products.

11.1.2 Keynes’ Law and the Macroeconomics of Demand

The alternative to Say’s law, with its emphasis on supply, can be named Keynes’ law: “Demand creates its own supply.” As a matter of historical accuracy, just as Jean-Baptiste Say never wrote down anything as simpleminded as Say’s law, John Maynard Keynes never wrote down Keynes’ law, but the law is a useful simplification that conveys a certain point of view.

When Keynes wrote his great work The General Theory of Employment, Interest, and Money during the Great Depression of the 1930s, he pointed out that during the Depression, the capacity of the economy to supply goods and services had not changed much. U.S. unemployment rates soared higher than 20% from 1933 to 1935, but the number of possible workers had not increased or decreased much. Factories were closed and shuttered, but machinery and equipment had not disappeared. Technologies that had been invented in the 1920s were not un-invented and forgotten in the 1930s. Thus, Keynes argued that the Great Depression—and many ordinary recessions as well—were not caused by a drop in the ability of the economy to supply goods as measured by labor, physical capital, or technology. He argued the economy often produced less than its full potential, not because it was technically impossible to produce more with the existing workers and machines, but because a lack of demand in the economy as a whole led to inadequate incentives for firms to produce. In such cases, he argued, the level of GDP in the economy was not primarily determined by the potential of what the economy could supply, but rather by the amount of total demand.

Keynes’ law seems to apply fairly well in the short run of a few months to a few years, when many firms experience either a drop in demand for their output during a recession or so much demand that they have trouble producing enough during an economic boom. However, demand cannot tell the whole macroeconomic story, either. After all, if demand was all that mattered at the macroeconomic level, then the government could make the economy as large as it wanted just by pumping up total demand through a large increase in the government spending component or by legislating large tax cuts to push up the consumption component. Economies do, however, face genuine limits to how much they can produce, limits determined by the quantity of labor, physical capital, technology, and the institutional and market structures that bring these factors of production together. These constraints on what an economy can supply at the macroeconomic level do not disappear just because of an increase in demand.

11.1.3 Combining Supply and Demand in Macroeconomics

Two insights emerge from this overview of Say’s law with its emphasis on macroeconomic supply and Keynes’ law with its emphasis on macroeconomic demand. The first conclusion, which is not exactly a hot news flash, is that an economic approach focused only on the supply side or only on the demand side can be only a partial success. Both supply and demand need to be taken into account. The second conclusion is that since Keynes’ law applies more accurately in the short run and Say’s law applies more accurately in the long run, the tradeoffs and connections between the three goals of macroeconomics may be different in the short run and the long run.

- Neoclassical economists emphasize Say’s law, which holds that supply creates its own demand.

- Keynesian economists emphasize Keynes’ law, which holds that demand creates its own supply.

- Many mainstream economists take a Keynesian perspective, emphasizing the importance of aggregate demand, for the short run, and a neoclassical perspective, emphasizing the importance of aggregate supply, for the long run.

Describe the mechanism by which supply creates its own demand.

Describe the mechanism by which demand creates its own supply.

What is Say’s law?

Do neoclassical economists believe in Keynes’ law or Say’s law?

11.2 Building a Model of Aggregate Demand and Aggregate Supply

To build a useful macroeconomic model, we need a model that shows what determines total supply or total demand for the economy, and how total demand and total supply interact at the macroeconomic level. This model is called the aggregate demand/aggregate supply model. This module will explain aggregate supply, aggregate demand, and the equilibrium between them. The following modules will discuss the causes of shifts in aggregate supply and aggregate demand.

11.2.1 The Aggregate Supply Curve and Potential GDP

Firms make decisions about what quantity to supply based on the profits they expect to earn. Profits, in turn, are also determined by the price of the outputs the firm sells and by the price of the inputs, like labor or raw materials, the firm needs to buy. Aggregate supply (AS) refers to the total quantity of output (i.e. real GDP) firms will produce and sell. The aggregate supply (AS) curve shows the total quantity of output (i.e. real GDP) that firms will produce and sell at each price level.

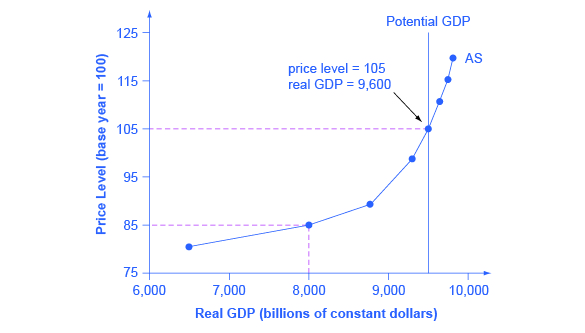

Figure 11.1 shows an aggregate supply curve. In the following paragraphs, we will walk through the elements of the diagram one at a time: the horizontal and vertical axes, the aggregate supply curve itself, and the meaning of the potential GDP vertical line.

The horizontal axis of the diagram shows real GDP—that is, the level of GDP adjusted for inflation. The vertical axis shows the price level. Remember that the price level is different from the inflation rate. Visualize the price level as an index number, like the GDP deflator, while the inflation rate is the percentage change between price levels over time.

As the price level (the average price of all goods and services produced in the economy) rises, the aggregate quantity of goods and services supplied rises as well. Why? The price level shown on the vertical axis represents prices for final goods or outputs bought in the economy—like the GDP deflator—not the price level for intermediate goods and services that are inputs to production. Thus, the AS curve describes how suppliers will react to a higher price level for final outputs of goods and services, while holding the prices of inputs like labor and energy constant. If firms across the economy face a situation where the price level of what they produce and sell is rising, but their costs of production are not rising, then the lure of higher profits will induce them to expand production.

The slope of an AS curve changes from nearly flat at its far left to nearly vertical at its far right. At the far left of the aggregate supply curve, the level of output in the economy is far below potential GDP, which is defined as the quantity that an economy can produce by fully employing its existing levels of labor, physical capital, and technology, in the context of its existing market and legal institutions. At these relatively low levels of output, levels of unemployment are high, and many factories are running only part-time, or have closed their doors. In this situation, a relatively small increase in the prices of the outputs that businesses sell—while making the assumption of no rise in input prices—can encourage a considerable surge in the quantity of aggregate supply because so many workers and factories are ready to swing into production.

Video - Aggregate Supply

As the quantity produced increases, however, certain firms and industries will start running into limits: perhaps nearly all of the expert workers in a certain industry will have jobs or factories in certain geographic areas or industries will be running at full speed. In the intermediate area of the AS curve, a higher price level for outputs continues to encourage a greater quantity of output—but as the increasingly steep upward slope of the aggregate supply curve shows, the increase in quantity in response to a given rise in the price level will not be quite as large. (Read the following Clear It Up feature to learn why the AS curve crosses potential GDP.)

WHY DOES AS-CURVE CROSS POTENTIAL GDP?

The aggregate supply curve is typically drawn to cross the potential GDP line. This shape may seem puzzling: How can an economy produce at an output level which is higher than its “potential” or “full employment” GDP? The economic intuition here is that if prices for outputs were high enough, producers would make fanatical efforts to produce: all workers would be on double-overtime, all machines would run 24 hours a day, seven days a week. Such hyper-intense production would go beyond using potential labor and physical capital resources fully, to using them in a way that is not sustainable in the long term. Thus, it is indeed possible for production to sprint above potential GDP, but only in the short run.

At the far right, the aggregate supply curve becomes nearly vertical. At this quantity, higher prices for outputs cannot encourage additional output, because even if firms want to expand output, the inputs of labor and machinery in the economy are fully employed. In this example, the vertical line in the exhibit shows that potential GDP occurs at a total output of 9,500. When an economy is operating at its potential GDP, machines and factories are running at capacity, and the unemployment rate is relatively low—at the natural rate of unemployment. For this reason, potential GDP is sometimes also called full-employment GDP.

11.2.2 The Aggregate Demand Curve

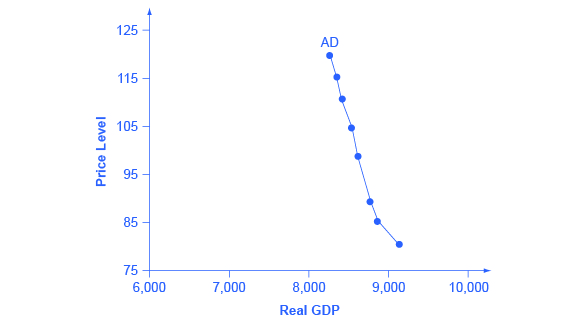

Aggregate demand (AD) refers to the amount of total spending on domestic goods and services in an economy. (Strictly speaking, AD is what economists call total planned expenditure. This distinction will be further explained in the appendix The Expenditure-Output Model . For now, just think of aggregate demand as total spending.) It includes all four components of demand: consumption, investment, government spending, and net exports (exports minus imports). This demand is determined by a number of factors, but one of them is the price level—recall though, that the price level is an index number such as the GDP deflator that measures the average price of the things we buy. The aggregate demand (AD) curve shows the total spending on domestic goods and services at each price level.

Figure 11.2 presents an aggregate demand (AD) curve. Just like the aggregate supply curve, the horizontal axis shows real GDP and the vertical axis shows the price level. The AD curve slopes down, which means that increases in the price level of outputs lead to a lower quantity of total spending. The reasons behind this shape are related to how changes in the price level affect the different components of aggregate demand. The following components make up aggregate demand: consumption spending (C), investment spending (I), government spending (G), and spending on exports (X) minus imports (M): C + I + G + X – M.

- The wealth effect holds that as the price level increases, the buying power of savings that people have stored up in bank accounts and other assets will diminish, eaten away to some extent by inflation. Because a rise in the price level reduces people’s wealth, consumption spending will fall as the price level rises.

- The interest rate effect is that as prices for outputs rise, the same purchases will take more money or credit to accomplish. This additional demand for money and credit will push interest rates higher. In turn, higher interest rates will reduce borrowing by businesses for investment purposes and reduce borrowing by households for homes and cars—thus reducing consumption and investment spending.

- The foreign price effect points out that if prices rise in the United States while remaining fixed in other countries, then goods in the United States will be relatively more expensive compared to goods in the rest of the world. U.S. exports will be relatively more expensive, and the quantity of exports sold will fall. U.S. imports from abroad will be relatively cheaper, so the quantity of imports will rise. Thus, a higher domestic price level, relative to price levels in other countries, will reduce net export expenditures.

Truth be told, among economists all three of these effects are controversial, in part because they do not seem to be very large. For this reason, the aggregate demand curve in Figure slopes downward fairly steeply; the steep slope indicates that a higher price level for final outputs reduces aggregate demand for all three of these reasons, but that the change in the quantity of aggregate demand as a result of changes in price level is not very large.

Read the following Work It Out feature to learn how to interpret the AD/AS model. In this example, aggregate supply, aggregate demand, and the price level are given for the imaginary country of Xurbia.

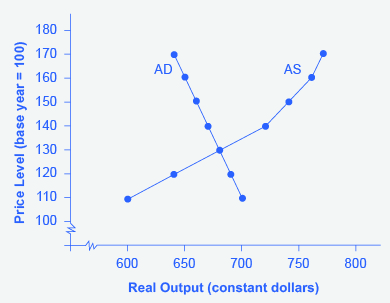

INTERPRETING THE AD/AS MODEL

The following table shows information on aggregate supply, aggregate demand, and the price level for the imaginary country of Xurbia. What information does Table tell you about the state of the Xurbia’s economy? Where is the equilibrium price level and output level (this is the SR macroequilibrium)? Is Xurbia risking inflationary pressures or facing high unemployment? How can you tell?

| Price Level | Aggregate Demand | Aggregate Supply |

|---|---|---|

| 110 | $700 | $600 |

| 120 | $690 | $640 |

| 130 | $680 | $680 |

| 140 | $670 | $720 |

| 150 | $660 | $740 |

| 160 | $650 | $760 |

| 170 | $640 | $770 |

To begin to use the AD/AS model, it is important to plot the AS and AD curves from the data provided. What is the equilibrium?

Step 1: Draw your x- and y-axis. Label the x-axis Real GDP and the y-axis Price Level.

Step 2: Plot AD on your graph.

Step 3: Plot AS on your graph.

Step 4: Look at Figure 11.3 which provides a visual to aid in your analysis.

Step 5: Determine where AD and AS intersect. This is the equilibrium with price level at 130 and real GDP at $680.

Step 6: Look at the graph to determine where equilibrium is located. We can see that this equilibrium is fairly far from where the AS curve becomes near-vertical (or at least quite steep) which seems to start at about $750 of real output. This implies that the economy is not close to potential GDP. Thus, unemployment will be high. In the relatively flat part of the AS curve, where the equilibrium occurs, changes in the price level will not be a major concern, since such changes are likely to be small.

Step 7: Determine what the steep portion of the AS curve indicates. Where the AS curve is steep, the economy is at or close to potential GDP.

Step 8: Draw conclusions from the given information:

- If equilibrium occurs in the flat range of AS, then economy is not close to potential GDP and will be experiencing unemployment, but stable price level.

- If equilibrium occurs in the steep range of AS, then the economy is close or at potential GDP and will be experiencing rising price levels or inflationary pressures, but will have a low unemployment rate.

11.2.3 Equilibrium in the Aggregate Demand/Aggregate Supply Model

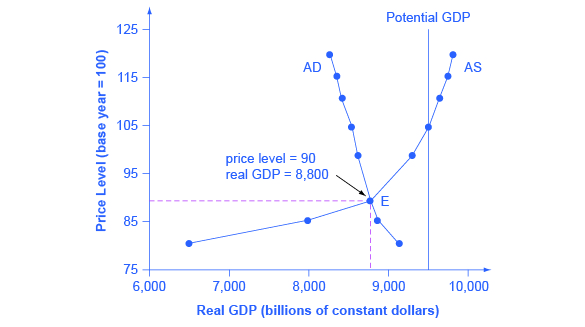

The intersection of the aggregate supply and aggregate demand curves shows the equilibrium level of real GDP and the equilibrium price level in the economy. At a relatively low price level for output, firms have little incentive to produce, although consumers would be willing to purchase a high quantity. As the price level for outputs rises, aggregate supply rises and aggregate demand falls until the equilibrium point is reached.

Figure Figure 11.4 combines the AS curve from Figure 11.1 and the AD curve from Figure 11.2 and places them both on a single diagram. In this example, the equilibrium point occurs at point E, at a price level of 90 and an output level of 8,800.

Confusion sometimes arises between the aggregate supply and aggregate demand model and the microeconomic analysis of demand and supply in particular markets for goods, services, labor, and capital. Read the following Clear It Up feature to gain an understanding of whether AS and AD are macro or micro.

ARE Aggregate Supply (AS) AND Aggregate Demand (AD) MACRO OR MICRO?

These aggregate supply and aggregate demand model and the microeconomic analysis of demand and supply in particular markets for goods, services, labor, and capital have a superficial resemblance, but they also have many underlying differences.

For example, the vertical and horizontal axes have distinctly different meanings in macroeconomic and microeconomic diagrams. The vertical axis of a microeconomic demand and supply diagram expresses a price (or wage or rate of return) for an individual good or service. This price is implicitly relative: it is intended to be compared with the prices of other products (for example, the price of pizza relative to the price of fried chicken). In contrast, the vertical axis of an aggregate supply and aggregate demand diagram expresses the level of a price index like the Consumer Price Index or the GDP deflator—combining a wide array of prices from across the economy. The price level is absolute: it is not intended to be compared to any other prices since it is essentially the average price of all products in an economy. The horizontal axis of a microeconomic supply and demand curve measures the quantity of a particular good or service. In contrast, the horizontal axis of the aggregate demand and aggregate supply diagram measures GDP, which is the sum of all the final goods and services produced in the economy, not the quantity in a specific market.

In addition, the economic reasons for the shapes of the curves in the macroeconomic model are different from the reasons behind the shapes of the curves in microeconomic models. Demand curves for individual goods or services slope down primarily because of the existence of substitute goods, not the wealth effects, interest rate, and foreign price effects associated with aggregate demand curves. The slopes of individual supply and demand curves can have a variety of different slopes, depending on the extent to which quantity demanded and quantity supplied react to price in that specific market, but the slopes of the AS and AD curves are much the same in every diagram (although as we shall see in later chapters, short-run and long-run perspectives will emphasize different parts of the AS curve).

In short, just because the AD/AS diagram has two lines that cross, do not assume that it is the same as every other diagram where two lines cross. The intuitions and meanings of the macro and micro diagrams are only distant cousins from different branches of the economics family tree.

11.2.4 Defining SRAS and LRAS

In the Clear It Up feature titled “Why does AS cross potential GDP?” we differentiated between short run changes in aggregate supply which are shown by the AS curve and long run changes in aggregate supply which are defined by the vertical line at potential GDP.

Video - Short-Run Aggregate Supply

In the short run, if demand is too low (or too high), it is possible for producers to supply less GDP (or more GDP) than potential.

In the long run, however, producers are limited to producing at potential GDP. For this reason, what we have been calling the AS curve, will from this point on may also be referred to as the short run aggregate supply (SRAS) curve. The vertical line at potential GDP may also be referred to as the long run aggregate supply (LRAS) curve.

The upward-sloping short run aggregate supply (SRAS) curve shows the positive relationship between the price level and the level of real GDP in the short run.

Aggregate supply slopes up because when the price level for outputs increases, while the price level of inputs remains fixed, the opportunity for additional profits encourages more production. The aggregate supply curve is near-horizontal on the left and near-vertical on the right.

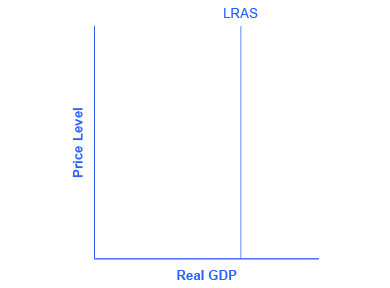

In the long run, aggregate supply is shown by a vertical line at the level of potential output, which is the maximum level of output the economy can produce with its existing levels of workers, physical capital, technology, and economic institutions.

The downward-sloping aggregate demand (AD) curve shows the relationship between the price level for outputs and the quantity of total spending in the economy. It slopes down because of:

- the wealth effect, which means that a higher price level leads to lower real wealth, which reduces the level of consumption;

- the interest rate effect, which holds that a higher price level will mean a greater demand for money, which will tend to drive up interest rates and reduce investment spending; and

- the foreign price effect, which holds that a rise in the price level will make domestic goods relatively more expensive, discouraging exports and encouraging imports.

The short run aggregate supply curve was constructed assuming that as the price of outputs increases, the price of inputs stays the same. How would an increase in the prices of important inputs, like energy, affect aggregate supply?

In the AD/AS model, what prevents the economy from achieving equilibrium at potential output?

What is on the horizontal axis of the AD/AS diagram? What is on the vertical axis?

11.3 Shifts in Aggregate Supply

The original equilibrium in the AD/AS diagram will shift to a new equilibrium if the AS or AD curve shifts. When the aggregate supply curve shifts to the right, then at every price level, a greater quantity of real GDP is produced. When the SRAS curve shifts to the left, then at every price level, a lower quantity of real GDP is produced. This module discusses two of the most important factors that can lead to shifts in the AS curve: productivity growth and input prices.

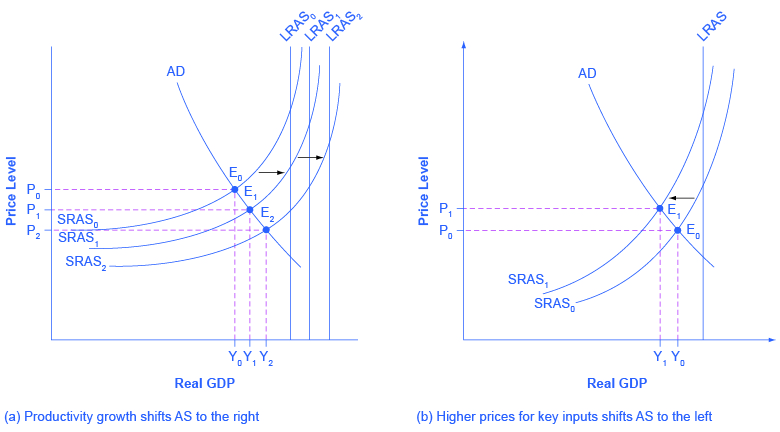

11.3.1 How Productivity Growth Shifts the AS Curve

In the long run, the most important factor shifting the AS curve is productivity growth. Productivity means how much output can be produced with a given quantity of labor. One measure of this is output per worker or GDP per capita. Over time, productivity grows so that the same quantity of labor can produce more output. Historically, the real growth in GDP per capita in an advanced economy like the United States has averaged about 2% to 3% per year, but productivity growth has been faster during certain extended periods like the 1960s and the late 1990s through the early 2000s, or slower during periods like the 1970s.

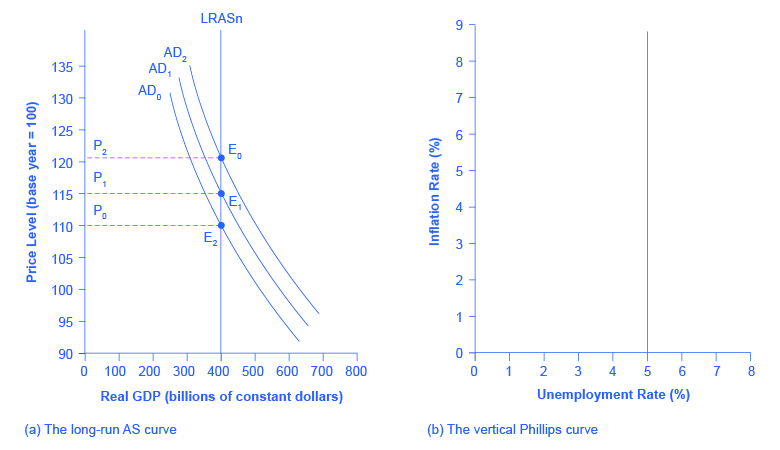

A higher level of productivity shifts the AS curve to the right, because with improved productivity, firms can produce a greater quantity of output at every price level. Figure 11.5 (a) shows an outward shift in productivity over two time periods. The AS curve shifts out from SRAS0 to SRAS1 to SRAS2, reflecting the rise in potential GDP in this economy, and the equilibrium shifts from E0 to E1 to E2.

A shift in the SRAS curve to the right will result in a greater real GDP and downward pressure on the price level, if aggregate demand remains unchanged. However, if this shift in SRAS results from gains in productivity growth, which are typically measured in terms of a few percentage points per year, the effect will be relatively small over a few months or even a couple of years.

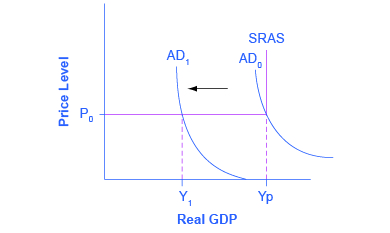

11.3.2 How Changes in Input Prices Shift the AS Curve

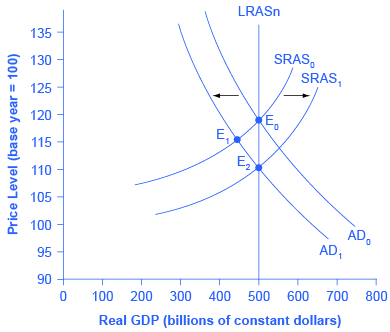

Higher prices for inputs that are widely used across the entire economy can have a macroeconomic impact on aggregate supply. Examples of such widely used inputs include wages and energy products. Increases in the price of such inputs will cause the SRAS curve to shift to the left, which means that at each given price level for outputs, a higher price for inputs will discourage production because it will reduce the possibilities for earning profits. Figure 11.5 (b) shows the aggregate supply curve shifting to the left, from SRAS0 to SRAS1, causing the equilibrium to move from E0 to E1.

The movement from the original equilibrium of E0 to the new equilibrium of E1 will bring a nasty set of effects: reduced GDP or recession, higher unemployment because the economy is now further away from potential GDP, and an inflationary higher price level as well. For example, the U.S. economy experienced recessions in 1974–1975, 1980–1982, 1990–91, 2001, and 2007–2009 that were each preceded or accompanied by a rise in the key input of oil prices. In the 1970s, this pattern of a shift to the left in SRAS leading to a stagnant economy with high unemployment and inflation was nicknamed stagflation.

Conversely, a decline in the price of a key input like oil will shift the SRAS curve to the right, providing an incentive for more to be produced at every given price level for outputs. From 1985 to 1986, for example, the average price of crude oil fell by almost half, from $24 a barrel to $12 a barrel. Similarly, from 1997 to 1998, the price of a barrel of crude oil dropped from $17 per barrel to $11 per barrel. In both cases, the plummeting price of oil led to a situation like that presented earlier in Figure 11.5 (a), where the outward shift of SRAS to the right allowed the economy to expand, unemployment to fall, and inflation to decline.

Along with energy prices, two other key inputs that may shift the SRAS curve are the cost of labor, or wages, and the cost of imported goods that are used as inputs for other products. In these cases as well, the lesson is that lower prices for inputs cause SRAS to shift to the right, while higher prices cause it to shift back to the left.

11.3.3 Other Supply Shocks

The aggregate supply curve can also shift due to shocks to input goods or labor. For example, an unexpected early freeze could destroy a large number of agricultural crops, a shock that would shift the AS curve to the left since there would be fewer agricultural products available at any given price.

Similarly, shocks to the labor market can affect aggregate supply. An extreme example might be an overseas war that required a large number of workers to cease their ordinary production in order to go fight for their country. In this case, aggregate supply would shift to the left because there would be fewer workers available to produce goods at any given price.

The aggregate demand/aggregate supply (AD/AS) diagram shows how AD and AS interact.

The intersection of the AD and AS curves shows the equilibrium output and price level in the economy. Movements of either AS or AD will result in a different equilibrium output and price level.

The aggregate supply curve will shift out to the right as productivity increases. It will shift back to the left as the price of key inputs rises, and will shift out to the right if the price of key inputs falls.

If the AS curve shifts back to the left, the combination of lower output, higher unemployment, and higher inflation, called stagflation, occurs.

If AS shifts out to the right, a combination of lower inflation, higher output, and lower unemployment is possible.

Suppose the U.S. Congress passes significant immigration reform that makes it easier for foreigners to come to the United States to work. Use the AD/AS model to explain how this would affect the equilibrium level of GDP and the price level.

Suppose concerns about the size of the federal budget deficit lead the U.S. Congress to cut all funding for research and development for ten years. Assuming this has an impact on technology growth, what does the AD/AS model predict would be the likely effect on equilibrium GDP and the price level?

Name some factors that could cause the SRAS curve to shift, and say whether they would shift SRAS to the right or to the left.

Will the shift of SRAS to the right tend to make the equilibrium quantity and price level higher or lower? What about a shift of SRAS to the left?

11.4 Shifts in Aggregate Demand

As mentioned previously, the components of aggregate demand are consumption spending (C), investment spending (I), government spending (G), and spending on exports (X) minus imports (M). (Read the following Clear It Up feature for explanation of why imports are subtracted from exports and what this means for aggregate demand.)

A shift of the AD curve to the right means that at least one of these components increased so that a greater amount of total spending would occur at every price level.

A shift of the AD curve to the left means that at least one of these components decreased so that a lesser amount of total spending would occur at every price level. The Keynesian Perspective will discuss the components of aggregate demand and the factors that affect them. Here, the discussion will sketch two broad categories that could cause AD curves to shift: changes in the behavior of consumers or firms and changes in government tax or spending policy.

DO IMPORTS DIMINISH AGGREGATE DEMAND?

We have seen that the formula for aggregate demand is AD = C + I + G + X - M, where M is the total value of imported goods. Why is there a minus sign in front of imports? Does this mean that more imports will result in a lower level of aggregate demand?

When an American buys a foreign product, for example, it gets counted along with all the other consumption. So the income generated does not go to American producers, but rather to producers in another country; it would be wrong to count this as part of domestic demand. Therefore, imports added in consumption are subtracted back out in the M term of the equation.

Because of the way in which the demand equation is written, it is easy to make the mistake of thinking that imports are bad for the economy. Just keep in mind that every negative number in the M term has a corresponding positive number in the C or I or G term, and they always cancel out.

11.4.1 How Changes by Consumers and Firms Can Affect AD

When consumers feel more confident about the future of the economy, they tend to consume more. If business confidence is high, then firms tend to spend more on investment, believing that the future payoff from that investment will be substantial. Conversely, if consumer or business confidence drops, then consumption and investment spending decline.

The University of Michigan publishes a survey of consumer confidence and constructs an index of consumer confidence each month. The survey results are then reported at http://www.sca.isr.umich.edu, which break down the change in consumer confidence among different income levels. According to that index, consumer confidence averaged around 90 prior to the Great Recession, and then it fell to below 60 in late 2008, which was the lowest it had been since 1980. Since then, confidence has climbed from a 2011 low of 55.8 back to a level in the low 80s, which is considered close to being considered a healthy state.

One measure of business confidence is published by the OECD: the "business tendency surveys". Business opinion survey data are collected for 21 countries on future selling prices and employment, among other elements of the business climate. After sharply declining during the Great Recession, the measure has risen above zero again and is back to long-term averages (the indicator dips below zero when business outlook is weaker than usual). Of course, either of these survey measures is not very precise. They can however, suggest when confidence is rising or falling, as well as when it is relatively high or low compared to the past.

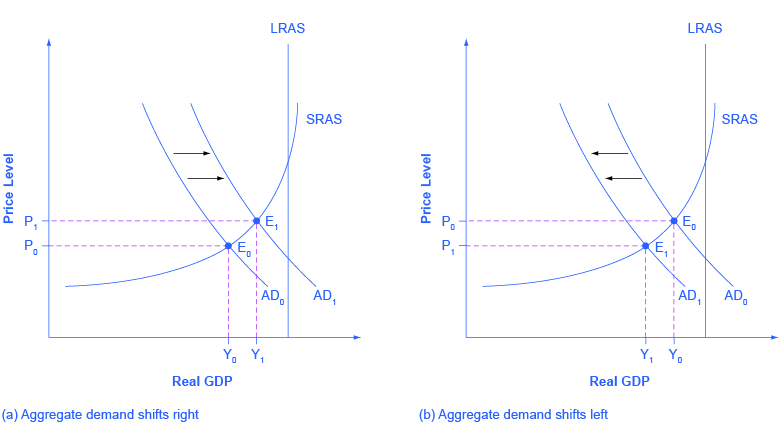

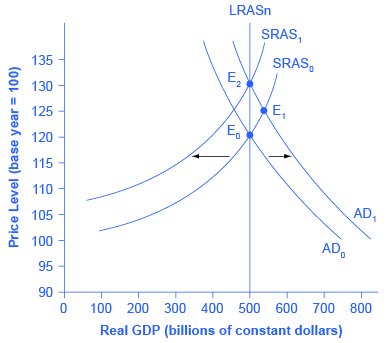

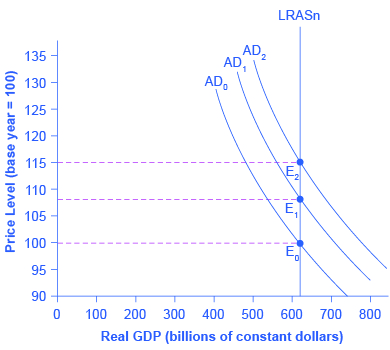

Because a rise in confidence is associated with higher consumption and investment demand, it will lead to an outward shift in the AD curve, and a move of the equilibrium, from E0 to E1, to a higher quantity of output and a higher price level, as shown in Figure 11.6 (a).

Consumer and business confidence often reflect macroeconomic realities; for example, confidence is usually high when the economy is growing briskly and low during a recession. However, economic confidence can sometimes rise or fall for reasons that do not have a close connection to the immediate economy, like a risk of war, election results, foreign policy events, or a pessimistic prediction about the future by a prominent public figure. U.S. presidents, for example, must be careful in their public pronouncements about the economy. If they offer economic pessimism, they risk provoking a decline in confidence that reduces consumption and investment and shifts AD to the left, and in a self-fulfilling prophecy, contributes to causing the recession that the president warned against in the first place. A shift of AD to the left, and the corresponding movement of the equilibrium, from E0 to E1, to a lower quantity of output and a lower price level, is shown in Figure 11.6 (b).

11.4.2 How Government Macroeconomic Policy Choices Can Shift AD

Government spending is one component of AD. Thus, higher government spending will cause AD to shift to the right, as in Figure (a), while lower government spending will cause AD to shift to the left, as in Figure (b). For example, in the United States, government spending declined by 3.2% of GDP during the 1990s, from 21% of GDP in 1991, and to 17.8% of GDP in 1998. However, from 2005 to 2009, the peak of the Great Recession, government spending increased from 19% of GDP to 21.4% of GDP. If changes of a few percentage points of GDP seem small to you, remember that since GDP was about $14.4 trillion in 2009, a seemingly small change of 2% of GDP is equal to close to $300 billion.

Tax policy can affect consumption and investment spending, too. Tax cuts for individuals will tend to increase consumption demand, while tax increases will tend to diminish it. Tax policy can also pump up investment demand by offering lower tax rates for corporations or tax reductions that benefit specific kinds of investment. Shifting C or I will shift the AD curve as a whole.

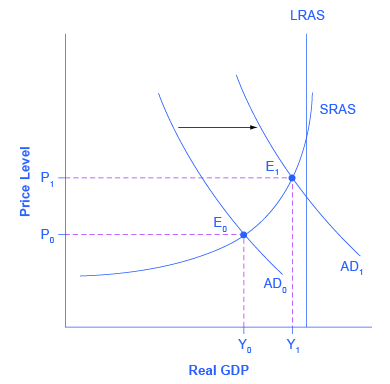

During a recession, when unemployment is high and many businesses are suffering low profits or even losses, the U.S. Congress often passes tax cuts. During the recession of 2001, for example, a tax cut was enacted into law. At such times, the political rhetoric often focuses on how people going through hard times need relief from taxes. The aggregate supply and aggregate demand framework, however, offers a complementary rationale, as illustrated in Figure. The original equilibrium during a recession is at point E0, relatively far from the full employment level of output. The tax cut, by increasing consumption, shifts the AD curve to the right. At the new equilibrium (E1), real GDP rises and unemployment falls and, because in this diagram the economy has not yet reached its potential or full employment level of GDP, any rise in the price level remains muted. Read the following Clear It Up feature to consider the question of whether economists favor tax cuts or oppose them.

DO ECONOMISTS FAVOR TAX CUTS OR OPPOSE THEM?

One of the most fundamental divisions in American politics over the last few decades has been between those who believe that the government should cut taxes substantially and those who disagree. Ronald Reagan rode into the presidency in 1980 partly because of his promise, soon carried out, to enact a substantial tax cut. George Bush lost his bid for reelection against Bill Clinton in 1992 partly because he had broken his 1988 promise: “Read my lips! No new taxes!” In the 2000 presidential election, both George W. Bush and Al Gore advocated substantial tax cuts and Bush succeeded in pushing a package of tax cuts through Congress early in 2001. Disputes over tax cuts often ignite at the state and local level as well.

What side are economists on? Do they support broad tax cuts or oppose them? The answer, unsatisfying to zealots on both sides, is that it depends. One issue is whether the tax cuts are accompanied by equally large government spending cuts. Economists differ, as does any broad cross-section of the public, on how large government spending should be and what programs might be cut back. A second issue, more relevant to the discussion in this chapter, concerns how close the economy is to the full employment level of output. In a recession, when the intersection of the AD and AS curves is far below the full employment level, tax cuts can make sense as a way of shifting AD to the right. However, when the economy is already doing extremely well, tax cuts may shift AD so far to the right as to generate inflationary pressures, with little gain to GDP.

With the AD/AS framework in mind, many economists might readily believe that the Reagan tax cuts of 1981, which took effect just after two serious recessions, were beneficial economic policy. Similarly, the Bush tax cuts of 2001 and the Obama tax cuts of 2009 were enacted during recessions. However, some of the same economists who favor tax cuts in time of recession would be much more dubious about identical tax cuts at a time the economy is performing well and cyclical unemployment is low.

Video - Shifts in Aggregate Demand and Supply

The use of government spending and tax cuts can be a useful tool to affect aggregate demand and it will be discussed in greater detail in the Government Budgets and Fiscal Policy chapter and The Impacts of Government Borrowing. Other policy tools can shift the aggregate demand curve as well. For example, as discussed in the Monetary Policy and Bank Regulation chapter, the Federal Reserve can affect interest rates and the availability of credit. Higher interest rates tend to discourage borrowing and thus reduce both household spending on big-ticket items like houses and cars and investment spending by business. Conversely, lower interest rates will stimulate consumption and investment demand. Interest rates can also affect exchange rates, which in turn will have effects on the export and import components of aggregate demand.

Spelling out the details of these alternative policies and how they affect the components of aggregate demand can wait for The Keynesian Perspective chapter. Here, the key lesson is that a shift of the aggregate demand curve to the right leads to a greater real GDP and to upward pressure on the price level. Conversely, a shift of aggregate demand to the left leads to a lower real GDP and a lower price level. Whether these changes in output and price level are relatively large or relatively small, and how the change in equilibrium relates to potential GDP, depends on whether the shift in the AD curve is happening in the relatively flat or relatively steep portion of the AS curve.

The AD curve will shift out as the components of aggregate demand—C, I, G, and X–M—rise. It will shift back to the left as these components fall. These factors can change because of different personal choices, like those resulting from consumer or business confidence, or from policy choices like changes in government spending and taxes. If the AD curve shifts to the right, then the equilibrium quantity of output and the price level will rise. If the AD curve shifts to the left, then the equilibrium quantity of output and the price level will fall. Whether equilibrium output changes relatively more than the price level or whether the price level changes relatively more than output is determined by where the AD curve intersects with the AS curve.

The AD/AS diagram superficially resembles the microeconomic supply and demand diagram on the surface, but in reality, what is on the horizontal and vertical axes and the underlying economic reasons for the shapes of the curves are very different. Long-term economic growth is illustrated in the AD/AS framework by a gradual shift of the aggregate supply curve to the right. A recession is illustrated when the intersection of AD and AS is substantially below potential GDP, while an expanding economy is illustrated when the intersection of AS and AD is near potential GDP.

How would a dramatic increase in the value of the stock market shift the AD curve? What effect would the shift have on the equilibrium level of GDP and the price level?

Suppose Mexico, one of our largest trading partners and purchaser of a large quantity of our exports, goes into a recession. Use the AD/AS model to determine the likely impact on our equilibrium GDP and price level.

A policymaker claims that tax cuts led the economy out of a recession. Can we use the AD/AS diagram to show this?

Many financial analysts and economists eagerly await the press releases for the reports on the home price index and consumer confidence index. What would be the effects of a negative report on both of these? What about a positive report?

11.5 How the AD/AS Model Incorporates Growth, Unemployment, and Inflation

The AD/AS model can convey a number of interlocking relationships between the four macroeconomic goals of growth, unemployment, inflation, and a sustainable balance of trade. Moreover, the AD/AS framework is flexible enough to accommodate both the Keynes’ law approach that focuses on aggregate demand and the short run, while also including the Say’s law approach that focuses on aggregate supply and the long run. These advantages are considerable.

Every model is a simplified version of the deeper reality and, in the context of the AD/AS model, the three macroeconomic goals arise in ways that are sometimes indirect or incomplete. In this module, we consider how the AD/AS model illustrates the three macroeconomic goals of economic growth, low unemployment, and low inflation.

11.5.1 Growth and Recession in the AD/AS Diagram

In the AD/AS diagram, long-run economic growth due to productivity increases over time will be represented by a gradual shift to the right of aggregate supply. The vertical line representing potential GDP (or the “full employment level of GDP”) will gradually shift to the right over time as well. A pattern of economic growth over three years, with the AS curve shifting slightly out to the right each year, was shown earlier in [link] (a). However, the factors that determine the speed of this long-term economic growth rate—like investment in physical and human capital, technology, and whether an economy can take advantage of catch-up growth—do not appear directly in the AD/AS diagram.

In the short run, GDP falls and rises in every economy, as the economy dips into recession or expands out of recession. Recessions are illustrated in the AD/AS diagram when the equilibrium level of real GDP is substantially below potential GDP, as occurred at the equilibrium point E0 in [link]. On the other hand, in years of resurgent economic growth the equilibrium will typically be close to potential GDP, as shown at equilibrium point E1 in that earlier figure.

11.5.2 Unemployment in the AD/AS Diagram

Two types of unemployment were described in the Unemployment chapter. Cyclical unemployment bounces up and down according to the short-run movements of GDP. Over the long run, in the United States, the unemployment rate typically hovers around 5% (give or take one percentage point or so), when the economy is healthy.

In many of the national economies across Europe, the rate of unemployment in recent decades has only dropped to about 10% or a bit lower, even in good economic years. This baseline level of unemployment that occurs year-in and year-out is called the natural rate of unemployment and is determined by how well the structures of market and government institutions in the economy lead to a matching of workers and employers in the labor market. Potential GDP can imply different unemployment rates in different economies, depending on the natural rate of unemployment for that economy.

In the AD/AS diagram, cyclical unemployment is shown by how close the economy is to the potential or full employment level of GDP. Returning to [link], relatively low cyclical unemployment for an economy occurs when the level of output is close to potential GDP, as in the equilibrium point E1. Conversely, high cyclical unemployment arises when the output is substantially to the left of potential GDP on the AD/AS diagram, as at the equilibrium point E0. The factors that determine the natural rate of unemployment are not shown separately in the AD/AS model, although they are implicitly part of what determines potential GDP or full employment GDP in a given economy.

11.5.3 Inflationary Pressures in the AD/AS Diagram

Inflation fluctuates in the short run. Higher inflation rates have typically occurred either during or just after economic booms: for example, the biggest spurts of inflation in the U.S. economy during the twentieth century followed the wartime booms of World War I and World War II. Conversely, rates of inflation generally decline during recessions. As an extreme example, inflation actually became negative—a situation called “deflation”—during the Great Depression.

Even during the relatively short recession of 1991–1992, the rate of inflation declined from 5.4% in 1990 to 3.0% in 1992. During the relatively short recession of 2001, the rate of inflation declined from 3.4% in 2000 to 1.6% in 2002. During the deep recession of 2007–2009, the rate of inflation declined from 3.8% in 2008 to –0.4% in 2009. Some countries have experienced bouts of high inflation that lasted for years. In the U.S. economy since the mid–1980s, inflation does not seem to have had any long-term trend to be substantially higher or lower; instead, it has stayed in the range of 1–5% annually.

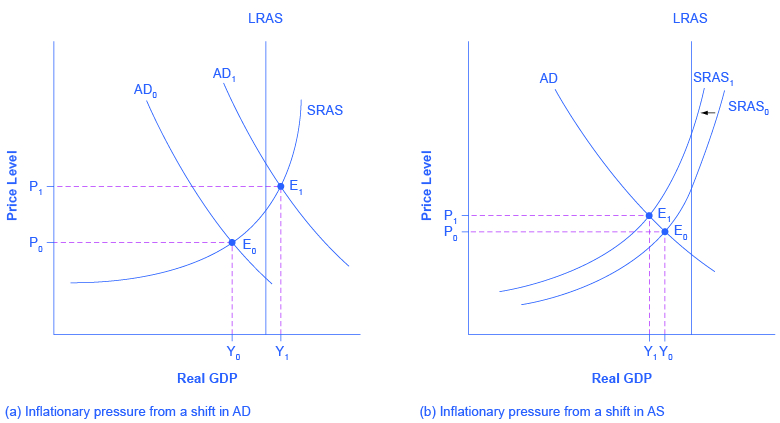

The AD/AS framework implies two ways that inflationary pressures may arise. One possible trigger is if aggregate demand continues to shift to the right when the economy is already at or near potential GDP and full employment, thus pushing the macroeconomic equilibrium into the steep portion of the AS curve. In Figure 11.8 (a), there is a shift of aggregate demand to the right; the new equilibrium E1 is clearly at a higher price level than the original equilibrium E0. In this situation, the aggregate demand in the economy has soared so high that firms in the economy are not capable of producing additional goods, because labor and physical capital are fully employed, and so additional increases in aggregate demand can only result in a rise in the price level.

An alternative source of inflationary pressures can occur due to a rise in input prices that affects many or most firms across the economy—perhaps an important input to production like oil or labor—and causes the aggregate supply curve to shift back to the left. In Figure 11.8 (b), the shift of the SRAS curve to the left also increases the price level from P0 at the original equilibrium (E0) to a higher price level of P1 at the new equilibrium (E1). In effect, the rise in input prices ends up, after the final output is produced and sold, being passed along in the form of a higher price level for outputs.

The AD/AS diagram shows only a one-time shift in the price level. It does not address the question of what would cause inflation either to vanish after a year, or to sustain itself for several years. There are two explanations for why inflation may persist over time. One way that continual inflationary price increases can occur is if the government continually attempts to stimulate aggregate demand in a way that keeps pushing the AD curve when it is already in the steep portion of the SRAS curve.

A second possibility is that, if inflation has been occurring for several years, a certain level of inflation may come to be expected. For example, if consumers, workers, and businesses all expect prices and wages to rise by a certain amount, then these expected rises in the price level can become built into the annual increases of prices, wages, and interest rates of the economy. These two reasons are interrelated, because if a government fosters a macroeconomic environment with inflationary pressures, then people will grow to expect inflation. However, the AD/AS diagram does not show these patterns of ongoing or expected inflation in a direct way.

11.5.4 Importance of the Aggregate Demand/Aggregate Supply Model

Macroeconomics takes an overall view of the economy, which means that it needs to juggle many different concepts. For example, start with the three macroeconomic goals of growth, low inflation, and low unemployment. Aggregate demand has four elements: consumption, investment, government spending, and exports less imports.

Aggregate supply reveals how businesses throughout the economy will react to a higher price level for outputs. Finally, a wide array of economic events and policy decisions can affect aggregate demand and aggregate supply, including government tax and spending decisions; consumer and business confidence; changes in prices of key inputs like oil; and technology that brings higher levels of productivity.

The aggregate demand/aggregate supply model is one of the fundamental diagrams in this course because it provides an overall framework for bringing these factors together in one diagram. Indeed, some version of the AD/AS model will appear in every chapter in the rest of this book.

Cyclical unemployment is relatively large in the AD/AS framework when the equilibrium is substantially below potential GDP.

Cyclical unemployment is small in the AD/AS framework when the equilibrium is near potential GDP.

The natural rate of unemployment, as determined by the labor market institutions of the economy, is built into what is meant by potential GDP, but does not otherwise appear in an AD/AS diagram.

Pressures for inflation to rise or fall are shown in the AD/AS framework when the movement from one equilibrium to another causes the price level to rise or to fall.

The balance of trade does not appear directly in the AD/AS diagram, but it appears indirectly in several ways. Increases in exports or declines in imports can cause shifts in AD. Changes in the price of key imported inputs to production, like oil, can cause shifts in AS.

The AD/AS model is the key model used in this book to understand macroeconomic issues.

What impact would a decrease in the size of the labor force have on GDP and the price level according to the AD/AS model?

Suppose, after five years of sluggish growth, the economy of the European Union picks up speed. What would be the likely impact on the U.S. trade balance, GDP, and employment?

Suppose the Federal Reserve begins to increase the supply of money at an increasing rate. What impact would that have on GDP, unemployment, and inflation?

11.6 Keynes’ Law and Say’s Law in the AD/AS Model

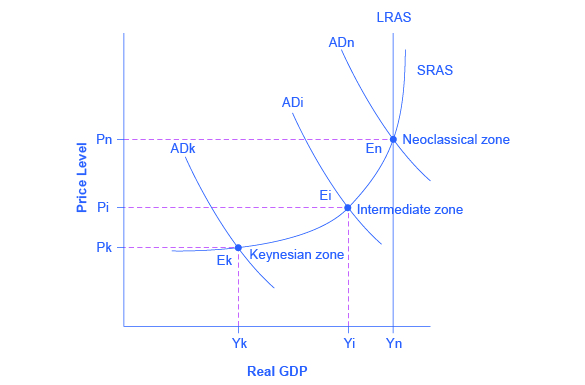

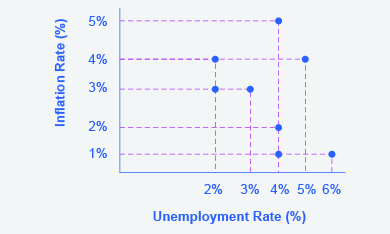

The AD/AS model can be used to illustrate both Say’s law that supply creates its own demand and Keynes’ law that demand creates its own supply. Consider the three zones of the SRAS curve as identified in Figure: the Keynesian zone, the neoclassical zone, and the intermediate zone.

Focus first on the Keynesian zone, that portion of the SRAS curve on the far left which is relatively flat. If the AD curve crosses this portion of the SRAS curve at an equilibrium point like Ek, then certain statements about the economic situation will follow. In the Keynesian zone, the equilibrium level of real GDP is far below potential GDP, the economy is in recession, and cyclical unemployment is high. If aggregate demand shifted to the right or left in the Keynesian zone, it will determine the resulting level of output (and thus unemployment). However, inflationary price pressure is not much of a worry in the Keynesian zone, since the price level does not vary much in this zone.

Now, focus your attention on the neoclassical zone of the SRAS curve, which is the near-vertical portion on the right-hand side. If the AD curve crosses this portion of the SRAS curve at an equilibrium point like En where output is at or near potential GDP, then the size of potential GDP pretty much determines the level of output in the economy. Since the equilibrium is near potential GDP, cyclical unemployment is low in this economy, although structural unemployment may remain an issue. In the neoclassical zone, shifts of aggregate demand to the right or the left have little effect on the level of output or employment. The only way to increase the size of the real GDP in the neoclassical zone is for AS to shift to the right. However, shifts in AD in the neoclassical zone will create pressures to change the price level.

Finally, consider the intermediate zone of the SRAS curve in Figure 11.9. If the AD curve crosses this portion of the SRAS curve at an equilibrium point like Ei, then we might expect unemployment and inflation to move in opposing directions. For instance, a shift of AD to the right will move output closer to potential GDP and thus reduce unemployment, but will also lead to a higher price level and upward pressure on inflation. Conversely, a shift of AD to the left will move output further from potential GDP and raise unemployment, but will also lead to a lower price level and downward pressure on inflation.

This approach of dividing the SRAS curve into different zones works as a diagnostic test that can be applied to an economy, like a doctor checking a patient for symptoms. First, figure out what zone the economy is in and then the economic issues, tradeoffs, and policy choices will be clarified. Some economists believe that the economy is strongly predisposed to be in one zone or another. Thus, hard-line Keynesian economists believe that the economies are in the Keynesian zone most of the time, and so they view the neoclassical zone as a theoretical abstraction. Conversely, hard-line neoclassical economists argue that economies are in the neoclassical zone most of the time and that the Keynesian zone is a distraction. The Keynesian Perspective and The Neoclassical Perspective should help to clarify the underpinnings and consequences of these contrasting views of the macroeconomy.

FROM HOUSING BUBBLE TO HOUSING BUST

Economic fluctuations, whether those experienced during the Great Depression of the 1930s, the stagflation of the 1970s, or the Great Recession of 2008–2009, can be explained using the AD/AS diagram. Short-run fluctuations in output occur due to shifts of the SRAS curve, the AD curve, or both. In the case of the housing bubble, rising home values caused the AD curve to shift to the right as more people felt that rising home values increased their overall wealth. Many homeowners took on mortgages that exceeded their ability to pay because, as home values continued to go up, the increased value would pay off any debt outstanding. Increased wealth due to rising home values lead to increased home equity loans and increased spending. All these activities pushed AD to the right, contributing to low unemployment rates and economic growth in the United States. When the housing bubble burst, overall wealth dropped dramatically, wiping out the recent gains. This drop in the value of homes was a demand shock to the U.S. economy because of its impact directly on the wealth of the household sector, and its contagion into the financial that essentially locked up new credit. The AD curve shifted to the left as evidenced by the rising unemployment of the Great Recession.

Understanding the source of these macroeconomic fluctuations provided monetary and fiscal policy makers with insight about what policy actions to take to mitigate the impact of the housing crisis. From a monetary policy perspective, the Federal Reserve lowered short-term interest rates to between 0% and 0.25 %, to loosen up credit throughout the financial system. Discretionary fiscal policy measures included the passage of the Emergency Economic Stabilization Act of 2008 that allowed for the purchase of troubled assets, such as mortgages, from financial institutions and the American Recovery and Reinvestment Act of 2009 that increased government spending on infrastructure, provided for tax cuts, and increased transfer payments. In combination, both monetary and fiscal policy measures were designed to help stimulate aggregate demand in the U.S. economy, pushing the AD curve to the right.

While most economists agree on the usefulness of the AD/AS diagram in analyzing the sources of these fluctuations, there is still some disagreement about the effectiveness of policy decisions that are useful in stabilizing these fluctuations. We discuss the possible policy actions and the differences among economists about their effectiveness in more detail in The Keynesian Perspective, Monetary Policy and Bank Regulation, and Government Budgets and Fiscal Policy.

The SRAS curve can be divided into three zones. Keynes’ law says demand creates its own supply, so that changes in aggregate demand cause changes in real GDP and employment. Keynes’ law can be shown on the horizontal Keynesian zone of the aggregate supply curve. The Keynesian zone occurs at the left of the SRAS curve where it is fairly flat, so movements in AD will affect output, but have little effect on the price level.

Say’s law says supply creates its own demand.

Changes in aggregate demand have no effect on real GDP and employment, only on the price level. Say’s law can be shown on the vertical neoclassical zone of the aggregate supply curve.

The neoclassical zone occurs at the right of the SRAS curve where it is fairly vertical, and so movements in AD will affect the price level, but have little impact on output. The intermediate zone in the middle of the SRAS curve is upward-sloping, so a rise in AD will cause higher output and price level, while a fall in AD will lead to a lower output and price level.

If the economy is operating in the neoclassical zone of the SRAS curve and aggregate demand falls, what is likely to happen to real GDP?

If the economy is operating in the Keynesian zone of the SRAS curve and aggregate demand falls, what is likely to happen to real GDP?

What is the Keynesian zone of the SRAS curve? How much is the price level likely to change in the Keynesian zone?

What is the neoclassical zone of the SRAS curve? How much is the output level likely to change in the neoclassical zone?

What is the intermediate zone of the SRAS curve? Will a rise in output be accompanied by a rise or a fall in the price level in this zone?

11.7 Aggregate Demand in Keynesian Analysis

THE GREAT RECESSION

The 2008-2009 Great Recession hit the U.S. economy hard. According to the Bureau of Labor Statistics (BLS), the number of unemployed Americans rose from 6.8 million in May 2007 to 15.4 million in October 2009. During that time, the U.S. Census Bureau estimated that approximately 170,000 small businesses closed. Mass layoffs peaked in February 2009 when employers gave 326,392 workers notice. U.S. productivity and output fell as well. Job losses, declining home values, declining incomes, and uncertainty about the future caused consumption expenditures to decrease. According to the BLS, household spending dropped by 7.8%.

Home foreclosures and the meltdown in U.S. financial markets called for immediate action by Congress, the President, and the Federal Reserve Bank. For example, the government implemented programs such as the American Restoration and Recovery Act to help millions of people by providing tax credits for homebuyers, paying “cash for clunkers,” and extending unemployment benefits. From cutting back on spending, filing for unemployment, and losing homes, millions of people were affected by the recession. While the United States is now on the path to recovery, people will feel the impact for many years to come.

What caused this recession and what prevented the economy from spiraling further into another depression? Policymakers looked to the lessons learned from the 1930s Great Depression and to John Maynard Keynes' models to analyze the causes and find solutions to the country’s economic woes. The Keynesian perspective is the subject of this chapter.

The Keynesian perspective focuses on aggregate demand. The idea is simple: firms produce output only if they expect it to sell. Thus, while the availability of the factors of production determines a nation’s potential GDP, the amount of goods and services that actually sell, known as real GDP, depends on how much demand exists across the economy. Figure 11.10 illustrates this point.

Keynes argued that, for reasons we explain shortly, aggregate demand is not stable—that it can change unexpectedly. Suppose the economy starts where AD intersects SRAS at P0 and Yp. Because Yp is potential output, the economy is at full employment. Because AD is volatile, it can easily fall. Thus, even if we start at Yp, if AD falls, then we find ourselves in what Keynes termed a recessionary gap. The economy is in equilibrium but with less than full employment, as Y1 in Figure shows. Keynes believed that the economy would tend to stay in a recessionary gap, with its attendant unemployment, for a significant period of time.

In the same way (although we do not show it in the figure), if AD increases, the economy could experience an inflationary gap, where demand is attempting to push the economy past potential output. Consequently, the economy experiences inflation. The key policy implication for either situation is that government needs to step in and close the gap, increasing spending during recessions and decreasing spending during booms to return aggregate demand to match potential output.

Recall from The Aggregate Supply-Aggregate Demand Model that aggregate demand is total spending, economy-wide, on domestic goods and services. (Aggregate demand (AD) is actually what economists call total planned expenditure. Read the appendix on The Expenditure-Output Model for more on this.) You may also remember that aggregate demand is the sum of four components: consumption expenditure, investment expenditure, government spending, and spending on net exports (exports minus imports). In the following sections, we will examine each component through the Keynesian perspective.

11.7.1 What Determines Consumption Expenditure?

Consumption expenditure is spending by households and individuals on durable goods, nondurable goods, and services. Durable goods are items that last and provide value over time, such as automobiles. Nondurable goods are things like groceries—once you consume them, they are gone. Recall from The Macroeconomic Perspective that services are intangible things consumers buy, like healthcare or entertainment.

Keynes identified three factors that affect consumption:

- Disposable income: For most people, the single most powerful determinant of how much they consume is how much income they have in their take-home pay, also known as disposable income, which is income after taxes.

- Expected future income: Consumer expectations about future income also are important in determining consumption. If consumers feel optimistic about the future, they are more likely to spend and increase overall aggregate demand. News of recession and troubles in the economy will make them pull back on consumption.

- Wealth or credit: When households experience a rise in wealth, they may be willing to consume a higher share of their income and to save less. When the U.S. stock market rose dramatically in the late 1990s, for example, U.S. savings rates declined, probably in part because people felt that their wealth had increased and there was less need to save. How do people spend beyond their income, when they perceive their wealth increasing? The answer is borrowing. On the other side, when the U.S. stock market declined about 40% from March 2008 to March 2009, people felt far greater uncertainty about their economic future, so savings rates increased while consumption declined.

Finally, Keynes noted that a variety of other factors combine to determine how much people save and spend. If household preferences about saving shift in a way that encourages consumption rather than saving, then AD will shift out to the right.

11.7.2 What Determines Investment Expenditure?

We call spending on new capital goods investment expenditure. Investment falls into four categories: producer’s durable equipment and software, nonresidential structures (such as factories, offices, and retail locations), changes in inventories, and residential structures (such as single-family homes, townhouses, and apartment buildings). Businesses conduct the first three types of investment, while households conduct the last.

Keynes’s treatment of investment focuses on the key role of expectations about the future in influencing business decisions. When a business decides to make an investment in physical assets, like plants or equipment, or in intangible assets, like skills or a research and development project, that firm considers both the expected investment benefits (future profit expectations) and the investment costs (interest rates).

- Expectations of future profits: The clearest driver of investment benefits is expectations for future profits. When we expect an economy to grow, businesses perceive a growing market for their products. Their higher degree of business confidence will encourage new investment. For example, in the second half of the 1990s, U.S. investment levels surged from 18% of GDP in 1994 to 21% in 2000. However, when a recession started in 2001, U.S. investment levels quickly sank back to 18% of GDP by 2002.

- Interest rates also play a significant role in determining how much investment a firm will make. Just as individuals need to borrow money to purchase homes, so businesses need financing when they purchase big ticket items. The cost of investment thus includes the interest rate. Even if the firm has the funds, the interest rate measures the opportunity cost of purchasing business capital. Lower interest rates stimulate investment spending and higher interest rates reduce it.

Many factors can affect the expected profitability on investment. For example, if the energy prices decline, then investments that use energy as an input will yield higher profits. If government offers special incentives for investment (for example, through the tax code), then investment will look more attractive; conversely, if government removes special investment incentives from the tax code, or increases other business taxes, then investment will look less attractive. As Keynes noted, business investment is the most variable of all the components of aggregate demand.

11.7.3 What Determines Government Spending?

The third component of aggregate demand is federal, state, and local government spending. Although we usually view the United States as a market economy, government still plays a significant role in the economy. As we discuss in Environmental Protection and Negative Externalities and Positive Externalitites and Public Goods, government provides important public services such as national defense, transportation infrastructure, and education.

Keynes recognized that the government budget offered a powerful tool for influencing aggregate demand. Not only could more government spending stimulate AD (or less government spending reduce it), but lowering or raising tax rates could influence consumption and investment spending. Keynes concluded that during extreme times like deep recessions, only the government had the power and resources to move aggregate demand.

11.7.4 What Determines Net Exports?

Recall that exports are domestically produced products that sell abroad while imports are foreign produced products that consumers purchase domestically. Since we define aggregate demand as spending on domestic goods and services, export expenditures add to AD, while import expenditures subtract from AD.

Two sets of factors can cause shifts in export and import demand: changes in relative growth rates between countries and changes in relative prices between countries. What is happening in the countries' economies that would be purchasing those exports heavily affects the level of demand for a nation's exports. For example, if major importers of American-made products like Canada, Japan, and Germany have recessions, exports of U.S. products to those countries are likely to decline. Conversely, the amount of income in the domestic economy directly affects the quantity of a nation's imports: more income will bring a higher level of imports.

Relative prices of goods in domestic and international markets can also affect exports and imports. If U.S. goods are relatively cheaper compared with goods made in other places, perhaps because a group of U.S. producers has mastered certain productivity breakthroughs, then U.S. exports are likely to rise. If U.S. goods become relatively more expensive, perhaps because a change in the exchange rate between the U.S. dollar and other currencies has pushed up the price of inputs to production in the United States, then exports from U.S. producers are likely to decline.

Table 11.1 summarizes the reasons we have explained for changes in aggregate demand.

| Reasons for a Decrease in Aggregate Demand | Reasons for an Increase in Aggregate Demand |

|---|---|

|

|

|

|

|

|

|

|

- Aggregate demand is the sum of four components: consumption, investment, government spending, and net exports.

- Consumption will change for a number of reasons, including movements in income, taxes, expectations about future income, and changes in wealth levels.

- Investment will change in response to its expected profitability, which in turn is shaped by expectations about future economic growth, the creation of new technologies, the price of key inputs, and tax incentives for investment.

- Investment will also change when interest rates rise or fall.

- Political considerations determine government spending and taxes.

- Exports and imports change according to relative growth rates and prices between two economies.

- In the Keynesian framework, which of the following events might cause a recession? Which might cause inflation? Sketch AD/AS diagrams to illustrate your answers.

- A large increase in the price of the homes people own.

- Rapid growth in the economy of a major trading partner.

- The development of a major new technology offers profitable opportunities for business.

- The interest rate rises.

- The good imported from a major trading partner become much less expensive.

- In a Keynesian framework, using an AD/AS diagram, which of the following government policy choices offer a possible solution to recession? Which offer a possible solution to inflation? a. A tax increase on consumer income. b. A surge in military spending. c. A reduction in taxes for businesses that increase investment. d. A major increase in what the U.S. government spends on healthcare.

- Name some economic events not related to government policy that could cause aggregate demand to shift.

11.8 The Building Blocks of Keynesian Analysis

Now that we have a clear understanding of what constitutes aggregate demand, we return to the Keynesian argument using the model of aggregate demand/aggregate supply (AD/AS). (For a similar treatment using Keynes’ income-expenditure model, see the appendix on The Expenditure-Output Model.)

Keynesian economics focuses on explaining why recessions and depressions occur and offering a policy prescription for minimizing their effects. The Keynesian view of recession is based on two key building blocks. First, aggregate demand is not always automatically high enough to provide firms with an incentive to hire enough workers to reach full employment. Second, the macroeconomy may adjust only slowly to shifts in aggregate demand because of sticky wages and prices, which are wages and prices that do not respond to decreases or increases in demand. We will consider these two claims in turn, and then see how they are represented in the AD/AS model.

The first building block of the Keynesian diagnosis is that recessions occur when the level of demand for goods and services is less than what is produced when labor is fully employed. In other words, the intersection of aggregate supply and aggregate demand occurs at a level of output less than the level of GDP consistent with full employment. Suppose the stock market crashes, as in 1929, or suppose the housing market collapses, as in 2008. In either case, household wealth will decline, and consumption expenditure will follow. Suppose businesses see that consumer spending is falling. That will reduce expectations of the profitability of investment, so businesses will decrease investment expenditure.

This seemed to be the case during the Great Depression, since the physical capacity of the economy to supply goods did not alter much. No flood or earthquake or other natural disaster ruined factories in 1929 or 1930. No outbreak of disease decimated the ranks of workers. No key input price, like the price of oil, soared on world markets. The U.S. economy in 1933 had just about the same factories, workers, and state of technology as it had had four years earlier in 1929—and yet the economy had shrunk dramatically. This also seems to be what happened in 2008.

As Keynes recognized, the events of the Depression contradicted Say’s law that “supply creates its own demand.” Although production capacity existed, the markets were not able to sell their products. As a result, real GDP was less than potential GDP.

11.8.1 Wage and Price Stickiness

Keynes also pointed out that although AD fluctuated, prices and wages did not immediately respond as economists often expected. Instead, prices and wages are “sticky,” making it difficult to restore the economy to full employment and potential GDP. Keynes emphasized one particular reason why wages were sticky: the coordination argument. This argument points out that, even if most people would be willing—at least hypothetically—to see a decline in their own wages in bad economic times as long as everyone else also experienced such a decline, a market-oriented economy has no obvious way to implement a plan of coordinated wage reductions. Unemployment proposed a number of reasons why wages might be sticky downward, most of which center on the argument that businesses avoid wage cuts because they may in one way or another depress morale and hurt the productivity of the existing workers.